本文來自格隆匯專欄:中金研究,作者:劉政寧、張文朗等

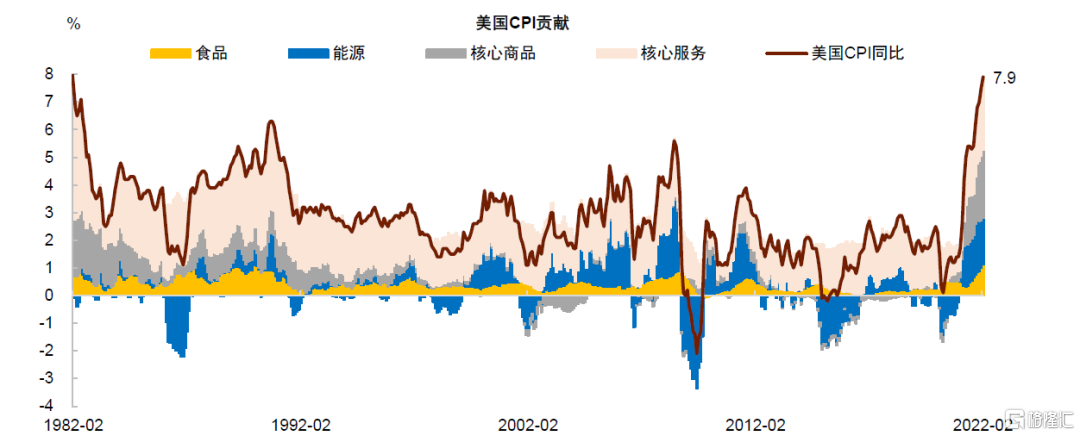

週四公佈的美國2月通脹率繼續上升,CPI同比增速升至7.9%,核心CPI同比增速升至6.4%。通脹高企或將加快美聯儲貨幣緊縮的節奏。另一方面,週四歐央行召開議息會議,顯著提高對2022年通脹的預測,並宣佈將以更快速度結束購債計劃(APP),為年底加息打開大門。我們認為,在通脹高企的背景下,海外各大央行的政策空間已經非常狹窄,留給他們的選項或許只有一個,那就是加快貨幣緊縮,對抗通脹。

美國方面,2月通脹保持強勁態勢,CPI指數環比增長0.8%,核心CPI指數環比增長0.5%,其中,核心CPI已經連續5個月環比增長高於0.5%,相當於年化6%。從分項看,汽油價格增長6.6%(環比,下同),食品價格增長1.0%,均呈現加速上漲趨勢。核心商品方面,前期漲幅較高的二手車價格下降0.2%,新車、服裝、傢俱、家電價格增速均有所放緩。核心服務方面,房租價格上漲0.5%,交通服務價格顯著上漲,顯示Omicron疫情消退後外出活動加快恢復。需要指出,2月通脹讀數中還不包括近期快速上漲的油價和小麥價格。3月1日以來,布倫特油價期貨價格和CBOT小麥期貨價格漲幅均在20%左右,這或意味着3月通脹將比2月更高,CPI同比增速突破8%的概率較大。

2月通脹數據強化了美聯儲加息的必要性,但更重要的是,美聯儲將以怎樣的節奏加息?我們曾在報吿《美聯儲加息指南》中討論了兩種加息路徑,分別是“小步快跑”和“大幹快上”式加息。“小步快跑”指美聯儲從3月起連續加息,直至年底,全年加息6次,每次加息幅度為25 bp。這種做法的好處是對資本市場衝擊相對小,缺點是難以很快控制通脹。“大幹快上”指在3、5、6月累計加息100 bp,之後視情況再加息,好處是能向市場展現抗通脹的決心,缺點是可能給資產價格造成衝擊。

儘管俄烏危機帶來不確定性,美聯儲仍可能“大幹快上”,一種可能是3月先加息25 bp,5月再加息50 bp,並在“縮表”議題上表現的更加積極。俄烏事件具有“滯脹”效應,對金融市場也造成一定衝擊,比如最近離岸美元互換利差FRA-OIS上升,表明市場流動性存在局部緊縮。出於金融穩定考慮,美聯儲可能在3月議息會議上先加息25 bp,同時暗示如果通脹居高不下,將在接下來的議息會議上加息50 bp。為控制通脹,美聯儲也可能進一步提前“縮表”,不排除在二季度末開啟“縮表”的可能性。

歐洲方面,歐央行態度超預期鷹派,不僅顯著上調通脹預測,還宣佈加快結束資產購買。我們預計歐央行最快將在四季度加息。根據歐央行最新預測,歐元區2022/23/24年GDP增速分別下調至3.7/2.8/1.6%,HICP通脹率分別上調至5.1/2.1/1.9%,核心HICP通脹率上調至2.6/1.8/1.9%。與美國不同,歐元區通脹高企主要因為能源價格高漲,歐洲能源供給對俄羅斯依賴度高,俄烏事件的發生無疑加大了通脹壓力。

資產購買方面,歐央行或在三季度結束APP資產購買計劃。歐央行宣佈,APP在4/5/6月的淨購買額將分別壓縮至400/300/200億歐元。而上次會議,歐央行的基準判斷是今年四季度之前可能都不會結束購債,由此可見,結束購債的時間已明顯提前。

加息方面,與上次會議相比,歐央行在政策聲明中刪除了“在加息不久前(shortly before)結束資產購買計劃”的措辭,將其改為“對歐洲央行關鍵利率的任何調整將在資產購買計劃結束一段時間後(some time after)進行,並將是漸進的”。這一變化在時間上解綁了購債結束與首次加息,強調了政策靈活性,但同時也給四季度加息提供可能。

總體上,歐央行對通脹的容忍度較上次會議明顯下降。儘管俄烏事件對歐洲帶來“滯脹”風險,但歐央行仍然選擇控制通脹,這也是我們認為歐央行超預期鷹派的一個重要原因。

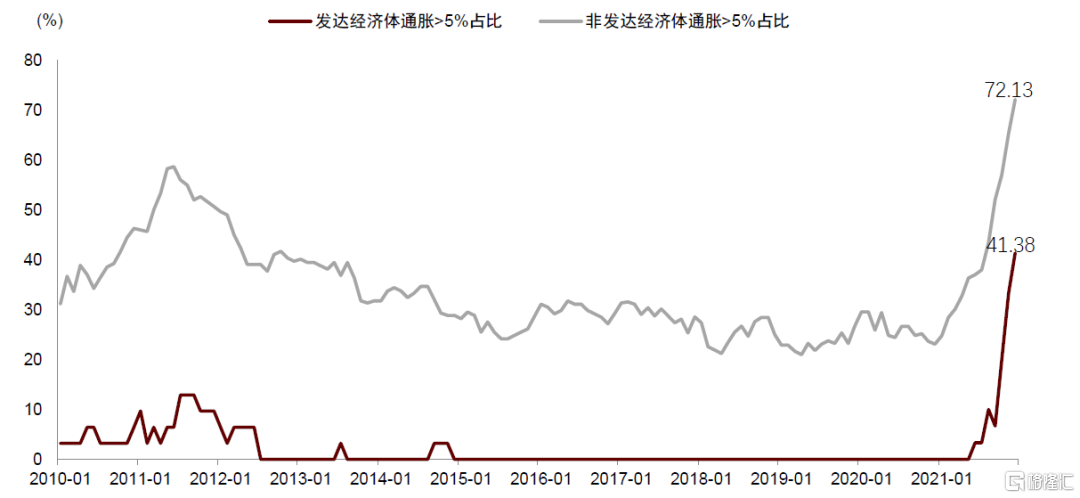

最後,通脹高企並非歐美獨有,其他發達國家和新興市場國家都存在高通脹現象。我們統計了全球範圍內CPI通脹高於5%的國家的數量。截止今年1月,在全球90個國家中,有56個國家通脹高於5%,佔比62%。其中,29個發達國家中,有12個國家通脹高於5%,佔比41%;61個發展中國家中,有44個國家通脹高於5%,佔比72%。也就是説,現在全球都處於一個高通脹的狀態,而且這裏只統計了CPI增速,如果看PPI增速,還要更高。從這個角度看,今年海外貨幣政策或出現集體“退潮”,海外央行緊縮將是今年最主要的宏觀風險之一。

圖表1:美國CPI通脹走勢及貢獻拆分

資料來源:Haver Analytics,中金公司研究部

圖表2:美國CPI通脹分行業數據概覽

資料來源:萬得資訊,中金公司研究部

圖表3:歐元區HICP通脹走勢及貢獻拆分

資料來源:Haver Analytics, 中金公司研究部

圖表4:全球通脹超過5%的國家佔比大幅上升

資料來源:IMF,中金公司研究部

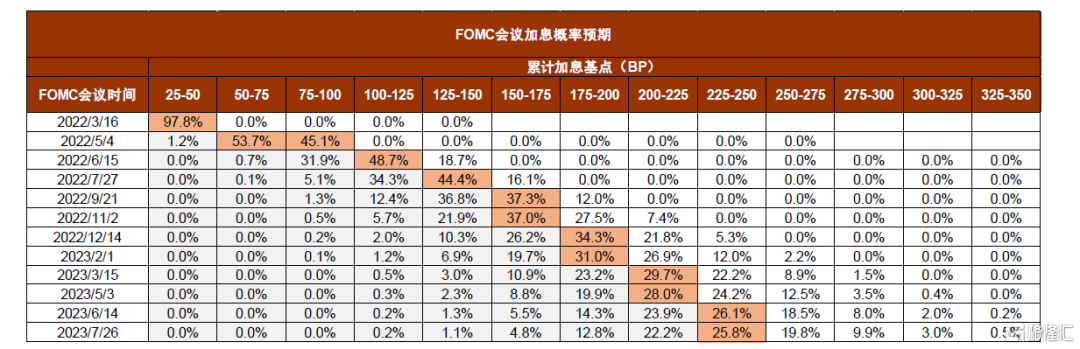

圖表5:美國2月通脹數據公佈後,市場預期的加息概率分佈

資料來源:CME Group,中金公司研究部。時間為2022年3月10日

More Content

Physical Store(set to open in Q2 2025)

Address:

Shop LMC 307, 3/F, Lok Ma Chau MTR Station, Lok Ma Chau

Opening Hour:

9am - 9pm (Mon - Sat)

10am - 6pm (Sun and Public Holiday)

(set to open in Q2 2025)