美國庫存重建對2022年中國出口的影響有多大?

本文來自:川閲全球宏觀,作者:陶川、趙藝原

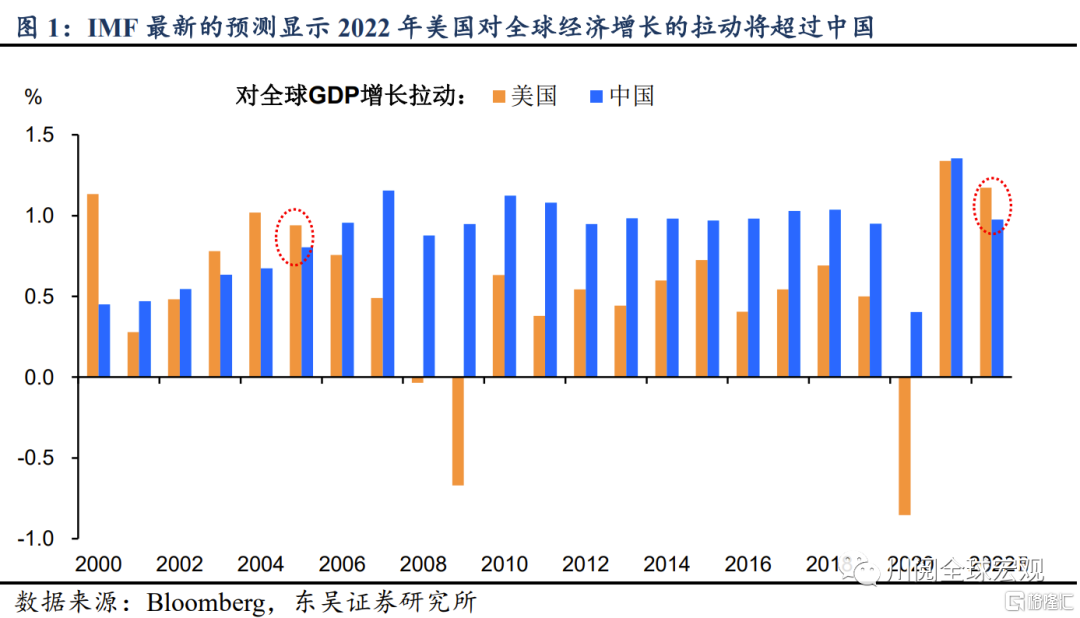

2021年以來雖然美國經濟強勁復甦,但中國得益於良好的疫情防控,在帶動全球經濟增長上依然強於美國。然而,2021年四季度以來隨着地產下行導致中國經濟下行壓力的加大,中國經濟的復甦開始出現分化。從當前來看,IMF預測2022年美國經濟對於全球經濟增長的拉動將超過中國,這還是2005年以來的第一次。

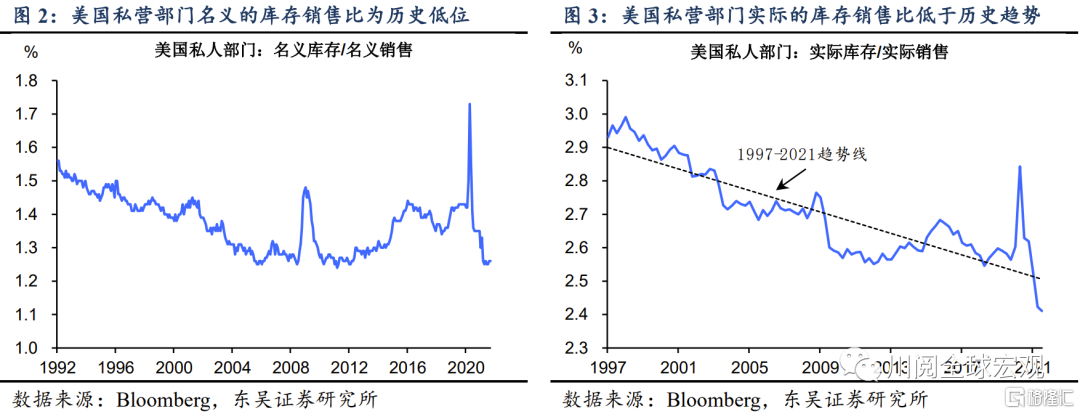

在財政刺激消退的背景下,美國經濟為何能在2022年引領全球經濟增長?我們認為其背後的一個重要原因是私人部門庫存的重建。如圖2-圖3所示,2021年由於疫情的反覆導致的供給短缺遲遲無法修復,美國私人部門在上半年進行了劇烈的去庫存以滿足需求激增;從當前來看,名義的庫存銷售比已經降至歷史低位,實際的庫存銷售比更是遠低於歷史趨勢線。因此,當前隨着供給瓶頸的逐步緩解,2022年美國私人部門的庫存重建應該是方興未艾。

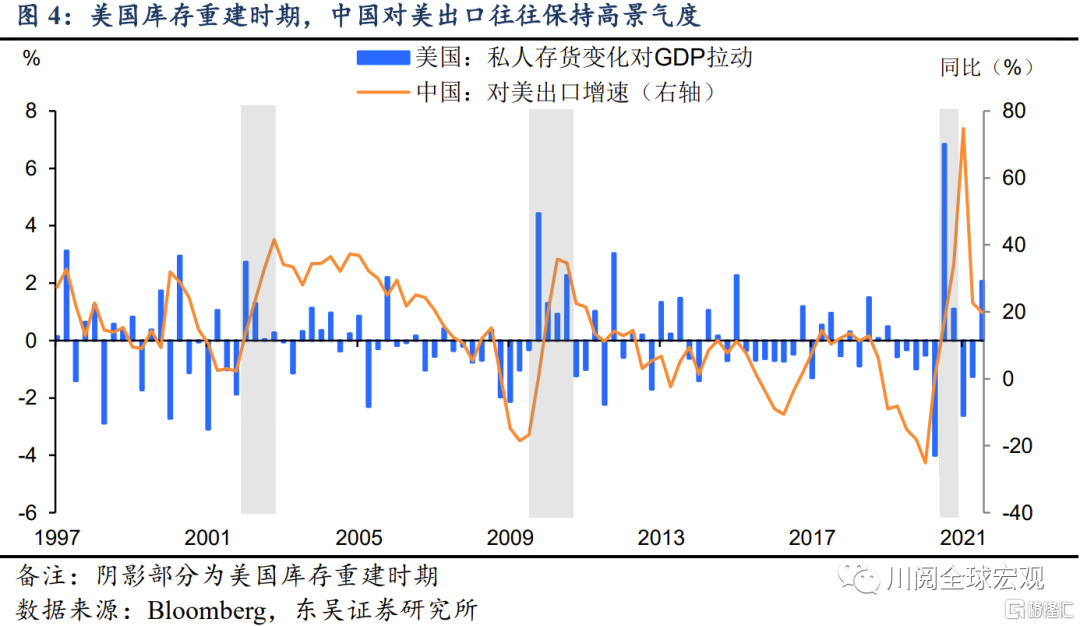

對中國經濟而言,2022年美國庫存重建將對中國的出口形成支撐。如圖4所示,歷史上當庫存重建持續拉動美國經濟增長時,中美對美出口的景氣度也保持高位,尤其是2002年和2009年Q4-2010年Q3,庫存重建對美國每個季度GDP增長的平均拉動在1-1.5個百分點,中國對美出口的增速始終保持在20%以上。鑑於2021年上半年美國去庫存的劇烈程度並不亞於這兩次庫存重建開啟前,我們預計在2022年,庫存重建對美國GDP增速的拉動有望超過1個百分點,成為僅次於私人消費的第二引擎,相應地,中國對美出口仍有望保持兩位數增長。

如何測算美國庫存重建對中國出口的拉動?

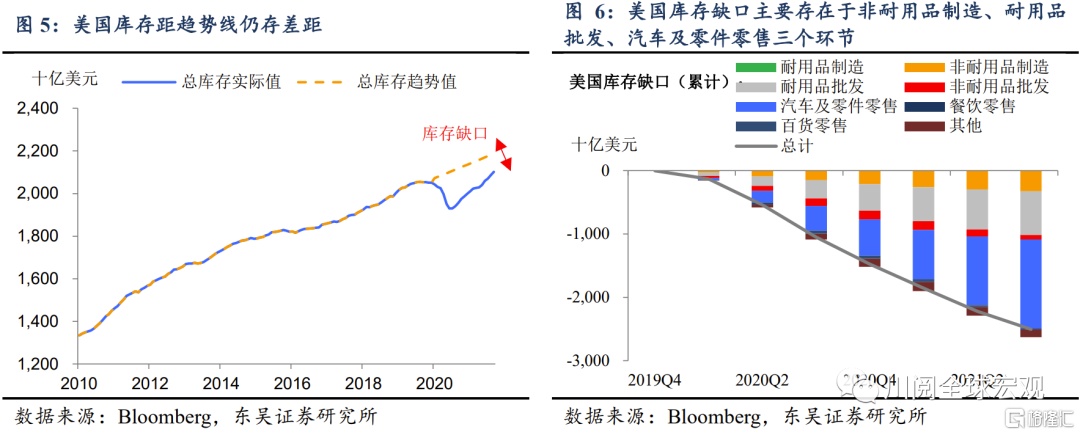

其一,當前美國庫存缺口規模有多大?我們計算了2020年以來美國三個部門(製造商、批發商、零售商)合計庫存距趨勢線的差距,截至2021年三季度,美國累計庫存缺口合計約為2.5萬億美元(圖5)。

其二,美國庫存缺口主要存在於什麼環節?如圖6所示,對三個部門進一步細分後,我們發現當前美國庫存缺口主要存在於非耐用品製造商、耐用品批發商、汽車零售商三個環節,截至2021年三季度,前述三個環節庫存缺口分別為3231億美元、6903億美元、1.4萬億美元。

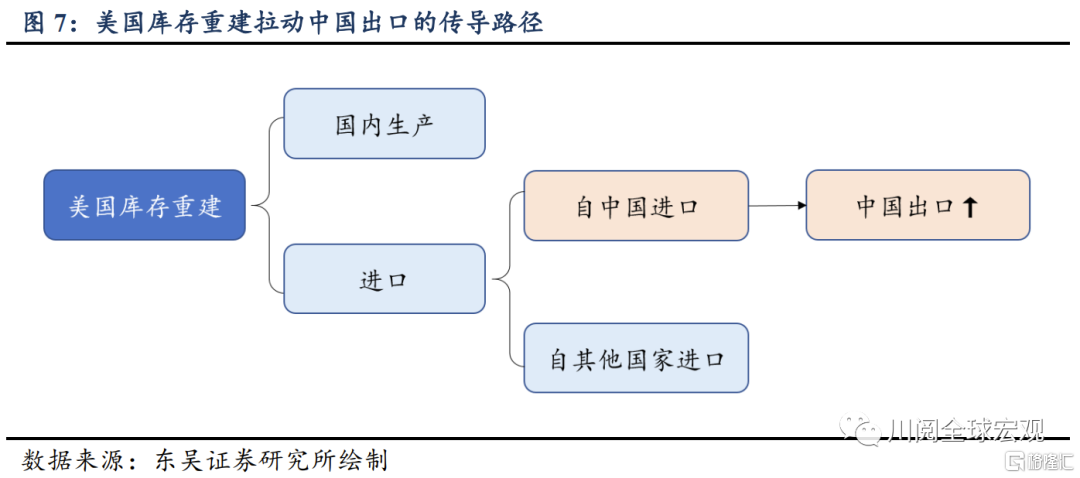

其三,美國補庫如何傳導至中國出口?我們以圖7展示美國補庫拉動中國出口的傳導路徑,即補庫來源分為美國國內生產和自他國進口,而進口中從中國進口的部分構成對中國出口的拉動。

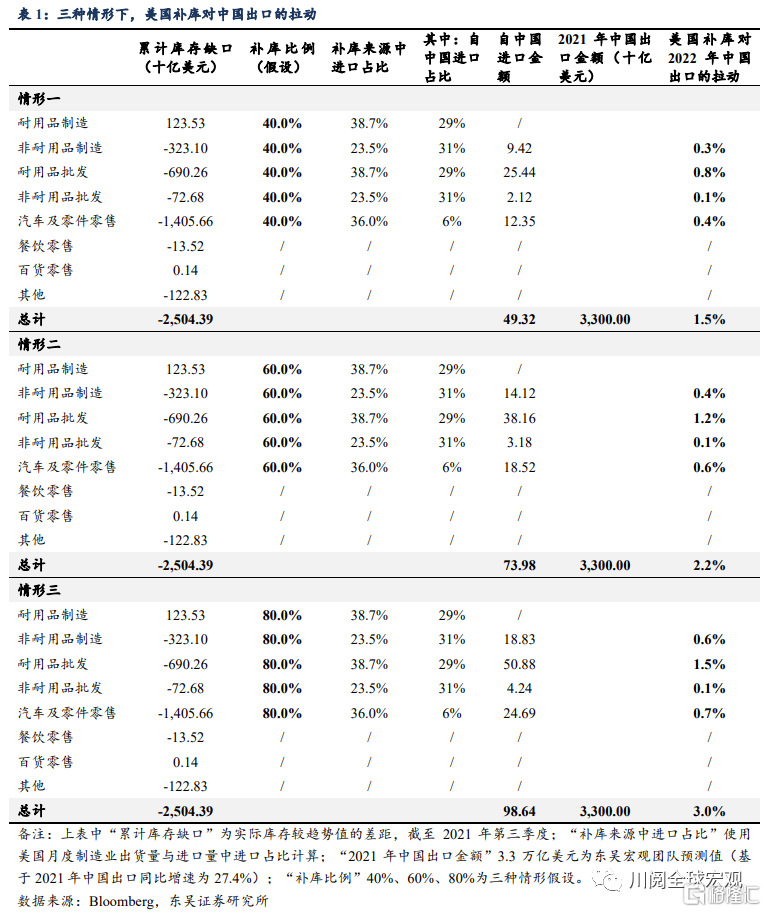

其四,補庫中進口占比多少?其中多少來自中國?我們使用美國月度製造業出貨量與進口量中進口占比計算相應產品的補庫進口比例(為簡化計算,我們僅對耐用品、非耐用品和汽車三類商品的補庫進口比例作區分);進口中多少來自中國則使用美國進口來源國分佈數據計算(為簡化計算,美國自中國進口的耐用品佔比使用機械設備+電氣設備進口數據作為參考,非耐用品使用服裝類產品進口數據作為參考。)

經過測算(表1),在2022年美國補庫比例分別為40%、60%、80%的三種情形下,美國補庫對中國出口的拉動分別為1.5個百分點、2.2個百分點、3.0個百分點。其中對中國對美出口的拉動分別為8.4個百分點、12.6個百分點、16.8個百分點。

由此可見,儘管高基數下2022年的中國出口面臨着放緩的壓力,但美國的庫存重建有望給中國出口增長帶來額外的動力,在這一拉動下,我們預計2022年中國出口增速仍將超過10%。

風險提示:全球疫情反覆延緩供給修復,美聯儲過早加息遏制經濟復甦

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of this article is for reference only. It does not constitute an offer, solicitation, recommendation, opinion or guarantee of any securities, financial products or instruments.The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance.