3月19日,恆安國際(01044.HK)公佈2020年年度業績。

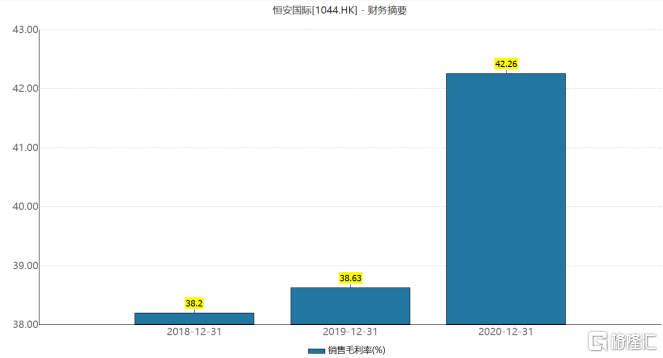

2020年全年,恆安國際錄得收入223.74億元,同比基本持平;毛利達到94.56億元,同比增長8.8%,毛利率由上年同期的38.6%升至42.3%;股東應占利潤為45.95億元,同比增長17.6%;每股基本收益約3.864元。董事會宣派末期股息每股1.30元,全年合共派息每股2.50元。

整體來看,疫情影響並未大幅波及恆安國際的全年業績表現,同時,在營收持平的情況下,其毛利、股東應占利潤均實現不俗增長,並延續了高比例的現金分紅。

四大業務板塊齊頭並進,拉動利潤大幅向好

具體到各個業務條線來看:

紙巾業務收入略有降低,毛利率顯著增長。基於國內商業及企業活動受疫情限制而對紙巾需求的削弱,以及會計準則下部分費用與收入的抵銷,恆安期內來自第一大業務紙巾的收入微降至103.83億元,佔集團整體收入約46.4%。而受惠於木漿成本仍處低位,紙巾業務毛利率顯著增長,由去年同期的27.7%升至約33.5%,同步帶動淨利潤的正向增長。

衞生巾業務重返升軌,展現潛在增長點。2020年,恆安衞生巾業務收入錄得近3.0%的同比增長,達到66.55元左右,高於年內市場平均增長水平,佔集團整體收入比例上升至約30.0%。其中,高端產品“Space7”實現快速增長,錄得收入約2億元,帶動衞生巾業務整體毛利率進一步升至約71.4%。財報同時透露,恆安正穩步邁向發展高端市場的策略,以擴大衞生巾市場份額,高端產品預計將成為集團在更長週期上的潛在增長點。

紙尿褲業務佈局漸見成效,降幅大幅收窄。受到渠道變遷的影響,恆安紙尿褲業務近年持續承壓。但至2020年,隨着恆安進一步加強在電商及母嬰銷售的佈局,以及高端嬰兒與成人紙尿褲產品的佔比提高,該業務錄得營收14.26億元左右,跌幅大幅收窄至約0.9%,佔集團整體收入保持約6.4%。尤其看到,高檔產品“Q•MO”的收入增幅超過70.0%,佔整體紙尿褲收入的額約18.9%。

其他收入及家居用品業務適時外延,實現多元創收。其他收入方面,恆安年內錄得收入39.11億元,同比增長約27.0%,當中包括因應疫情推出的口罩及其他醫療用相關產品。家居用品方面,恆安年內錄得收入約4.00億元,同比穩中有增,當中包括聲科集團收入約2.77億元。

業務高端化+外延化,深入把握行業增長機遇

基於恆安的這份財報,可以看到其兩大尤為關鍵的發展趨勢:高端化、外延化。

結合當前宏觀層面上,“需求側改革”(消費升級+消費擴容)力度的加大,以及人們對生活質量的追求提高,對日用消費品精細化訴求的不可逆性,我們認為,這也會是恆安未來長期價值積蓄的核心邏輯所在。

先聚焦高端化,如上文所述,恆安的高端衞生巾、紙尿褲業務等期內已取得不錯的成效,足以帶動整個業務板塊,甚至集團實現正向發展,未來潛力勢必不容小覷。一方面,高端化對恆安整體毛利率的提升將大有裨益;另一方面,高端化有助於恆安塑造更加豐富的產品矩陣,提供差異化、個性化的產品選擇,進而擴大集團的受眾羣體。基礎之上,消費升級為日用消費品的高端化趨勢提供出良好的發展條件,有望加速其發揮效能。

(來源:Wind)

外延化方面,筆者關注到兩大維度:

其一,產品品類的外延。例如,“心相印”品牌年內大幅擴產產品類型,先後推出了膠袋(包括垃圾袋及即棄手套)、食物保鮮膜、洗潔精、紙杯等。

行業維度上,多重因素激發中國日化市場呈現持續增長,據灼識諮詢,這一行業的零售額預計將於2024年增至8873億元,成長紅利依然可觀,不少細分領域也並未形成寡頭競爭,仍極具挖掘價值。凱度消費者指數《2020亞洲品牌足跡報吿》顯示,“心相印”在2019年以觸及消費者3.62億、滲透率59.7%,入圍中國快消品品牌前十。基於“心相印”強大的品牌力,恆安在切入更多日用品細分賽道上具有一定先發優勢。

其二,覆蓋市場的外延。恆安一直積極發展海外市場,集團產品目前已銷往42個國家及地區,擁有68個直接合作大客户或經銷商。業績方面,海外業務(包括皇城集團業務)全年營業額約21.67億元,佔集團整體收入的比例約9.7%,兩項指標較上年同期均有所提升。

基於2020年疫情的限制因素,海外消費市場中,本地供應商的競爭力在某種程度上被削弱,出海玩家迎來“彎道超車”機遇,順勢打響品牌知名度。中長週期來看,全球製造業處於重構競爭優勢的關鍵節點,實力企業有望在這股“暖風”下增強在海外市場的話語權,為未來的深耕奠定堅實基礎。因此,有理由認為,恆安的海外市場收入規模及佔比仍有望進一步提升,共助其實現持續高成長。

More Content

Physical Store(set to open in Q2 2025)

Address:

Shop LMC 307, 3/F, Lok Ma Chau MTR Station, Lok Ma Chau

Opening Hour:

9am - 9pm (Mon - Sat)

10am - 6pm (Sun and Public Holiday)

(set to open in Q2 2025)