騰訊控股(0700.HK):新業務快速發展,廣告下行

作者:王學恆

來源: 學恆的海外觀察

報告摘要

01

收入低於預期,廣告增速持續下行

三季度收入同比增長21%,至972億元,低於市場預期。今年廣告業務從一季度就略低於預期,三季度加速下行。這反應了:1、來自頭條的競爭;2、中國宏觀經濟承壓的現狀。三季度廣告收入增速僅為13%,創公司上市以來的新低水平。其中社交廣告32%的增長,媒體廣告同比下降28%。按照我們對於宏觀經濟的判斷,料Q4的廣告增速將成為增速的低點。

02

遊戲韌性強,海外遊戲有望成為新增長點

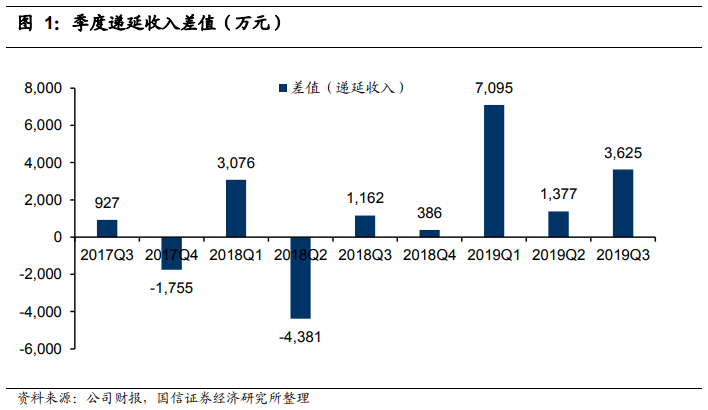

遊戲業務保持穩定的增長,手機遊戲同比增長25%,網絡遊戲同比增長11%。主要是王者榮耀的基本盤穩定,《和平精英》亦獲得不菲收益,遞延收入較Q2有明顯提升,三季度以來,海外遊戲增長較快,《PUBG MOBILE》的月活躍賬户數同比增長一倍,《Call of Duty Mobile》下載量超過1億。

03

支付與雲業務保持較快增長

三季度支付與雲保持了較快的增長,增速為36%,同時,雲收入同比增長80%至47億元。我們看到,隨着今年支付業務競爭趨緩,騰訊支付寶在商户返傭折扣降低,同時公司積極開展增值業務,使得支付業務毛利率穩健提升,這為明後年支付業務盈利的規模提升奠定基礎。

04

投資建議

我們小幅下調2019-2020年收入增速為22%(0pct)、20%(-1pct),淨利潤增速至23%、17%(持平),預計廣告業務觸底約在Q4,2019、2020年的EPS為港幣11.1元、13.7元,考慮人民幣升值,且經濟觸底回升廣告將回暖,我們維持增持評級,及維持目標估值區間380至400港幣,當前股價對應2019-2020年的PE為27X,23X。

05

風險提示

宏觀經濟的不確定性對廣告業務帶來的不利影響,遊戲增長不達預期。

報告正文

一、收入低於預期,遊戲保持良好韌性,廣告業務下行

三季度收入增長21%,至972億元,低於市場預期。廣告業務從一季度就略低於預期,三季度加速下行。這總體反應了1、來自頭條的競爭;2、中國宏觀經濟承壓的現狀。三季度廣告收入增速僅為13%,創公司上市以來的新低水平。其中社交廣告32%的增長,媒體廣告同比下降28%。按照我們對於宏觀經濟的判斷,料Q4的廣告增速可能成為增速的低點。

遊戲業務保持穩定的增長,手機遊戲同比增長25%,網絡遊戲同比增長11%。主要是王者榮耀的基本盤穩定,《和平精英》亦獲得不菲收益,遞延收入較Q2有明顯提升,Q3以來,海外遊戲增長較快,《PUBG MOBILE》的月活躍賬户數同比增長一倍,《Call of Duty Mobile》下載量超過1億。

三季度支付與雲保持了較快的增長,增速為36%,同時,雲收入同比增長80%至47億元。可喜的是,支付業務毛利率穩健提升,這為明後年支付業務的盈利的規模提升奠定基礎。

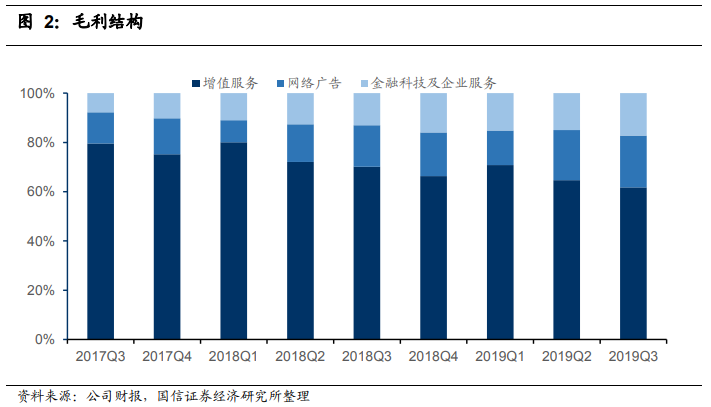

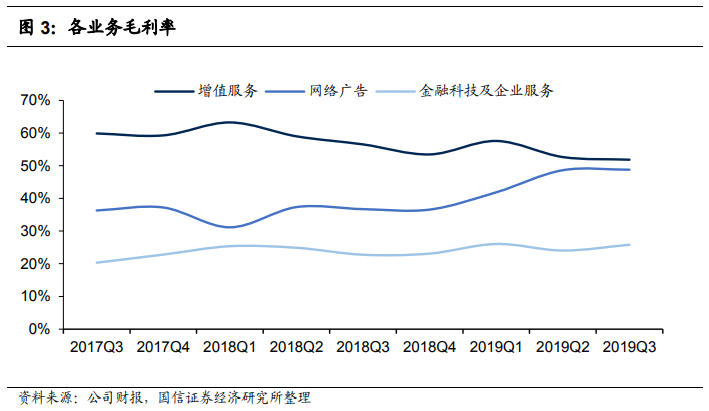

從毛利水平來看,三季度增值業務的毛利率基本持平,至51.8%;而廣告業務由於減少了宣傳費用,毛利率繼續維持高位至48.8%;支付與雲業務的毛利率25.8%,提升1個百分點。

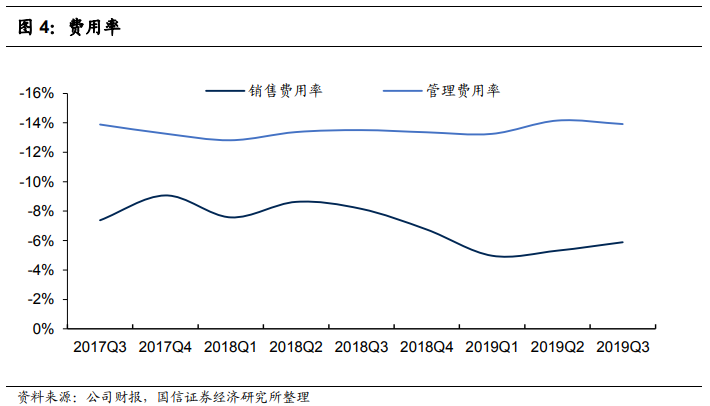

銷售費用率與管理費用率保持穩定。

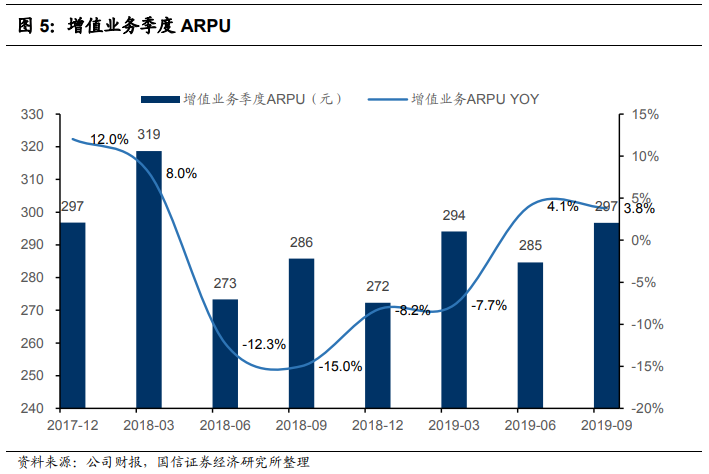

從增值業務ARPU值的增長率來看(相當於遊戲的CPI),在上個季度轉正的基礎上,本季度同比略有下滑,但依然保持在4%左右。我們一直提及,該指標是騰訊遊戲及增值業務的基本觀察指標,去年Q3-Q4在底部時,股價也下行明顯,而今年一季度開始快速反彈,股價也有明顯的一撥上漲。

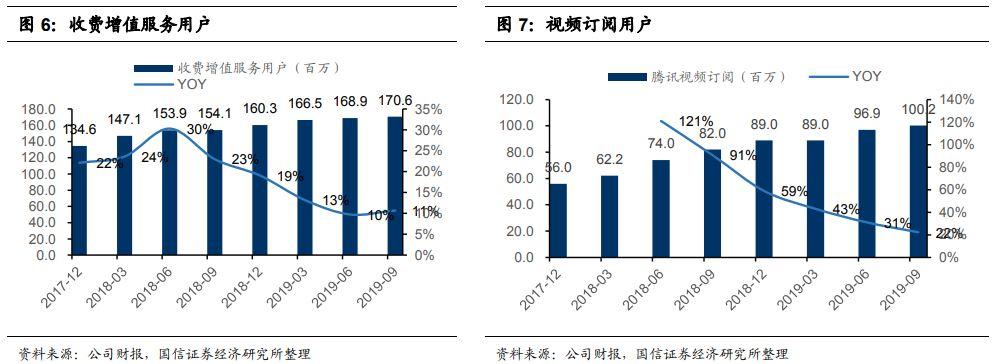

視頻訂閲用户同比增長22%,用户數首次過億;騰訊音樂用户數同比增長42%至3540萬户。

二、投資建議與風險提示

投資建議

我們小幅下調2019-2020年收入增速為22%(0pct)、20%(-1pct),淨利潤增速至23%、17%(持平),預計廣告業務觸底約在Q4,2019、2020年的EPS為港幣11.1元、13.7元,考慮人民幣升值,且經濟觸底回升廣告將回暖,我們維持增持評級,及維持目標估值區間380至400港幣,當前股價對應2019-2020年的PE為27X,23X。

風險提示

宏觀經濟的不確定性對廣告業務帶來的不利影響,遊戲增長不達預期。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of this article is for reference only. It does not constitute an offer, solicitation, recommendation, opinion or guarantee of any securities, financial products or instruments.The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance.