机构:银河证券

评级:增持

目标价:无

■ 在 2019 上半年,联邦制药基本上没有重大消息,股价大致窄幅上落。但我们认为,股 份今年稍后时间可能会获得重估,因为更多迹象显示公司正在从低端中间体和散装药生 产商转型为胰岛素生产商(预计胰岛素在 2019 年贡献超过 30%利润)。

■ 由于 2019 上半年 6APA 价格较低(约 145 元人民币/公斤,对比 2018 上半年为 206 元 人民币/公斤),因此我们估计 2019 上半年营业利润同比下降约 20%。到 2019 下半年, 上述影响将明显淡化,这是因为 2018 下半年的基数较低。

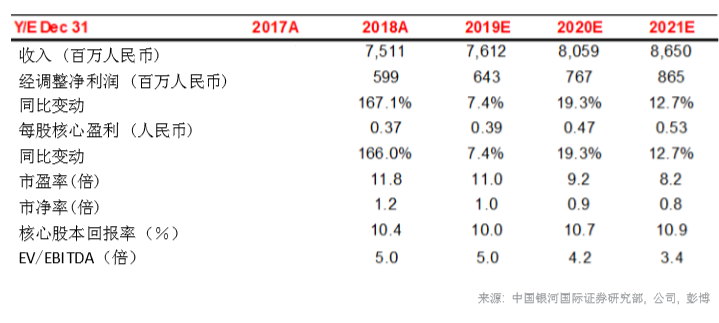

■ 总体而言,我们将 2019/2020/2021 年盈利预测分别下调 6.8%/2.9%/ 3.2%,主要是反 映中间体业务较弱的表现。

■ 我们的目标价是基于分类加总估值法所得出。考虑到公司同业的估值在近几个月下跌, 我们亦下调了联邦制药各个业务的估值。我们将目标价由 7.13 港元下调至 5.53 港元(相 当于 14.1/11.8/10.4 倍 2019/20/21 年市盈率)。

■ 维持「增持」评级,这是考虑到:1)在 2019 下半年的重新估值潜力;2)股份目前估 值不高,2019/20/21 年市盈率为 11.0/9.2/8.2 倍,预期 2018 - 2021 年每股盈利年复合 增长率达 13%。催化剂包括:1)甘精胰岛素销售快速提升;2)预计 2019 年末推出门 冬胰岛素注射液;3)公司有机会出售成都的投资物业,这将增强公司的资产负债表。

预计 6-APA 价格见底 根据 WIND,6-APA 价格(含增值税)从 2019 年一季度的 170-180 元人民币/公斤进一步 降至同年二季度 155-165 元人民币/公斤。我们认为这可能是由于国药集团威奇达药业恢复 500 吨/月的供应。展望未来,我们预计 2019 年的 6-APA 价格(含增值税)将维持持约 150 元人民币/公斤(低于我们之前估计的 180 元人民币/公斤)。目前的价格或已接近见底,因 为整个 6 -APA 行业(即联邦制药、四川科伦药业和威奇达)现阶段只录得轻微盈利。 我 们估计,由于 2019 年上半年 6-APA 价格较低(约 145 元人民币/公斤 vs. 2018 上半年为 206 元人民币/公斤),联邦制药 2019 年上半年营业利润将下降约 20%。为缓和 6-APA 价 格下降的影响,联邦制药减少了 6-APA 的对外销售,并且销售更多的阿莫西林原料药,其 平均售价在 2019 年上半年大致持稳于约 190 元人民币/公斤。

下调二代胰岛素的预测,但上调三代胰岛素的预测 鉴于未来几年竞争激烈,我们预计二代胰岛素收入可实现约 20%复合年增长率(低于我们 之前预测约 25%)。由于公司更积极进行学术推广,我们预计公司的三代胰岛素甘精胰岛 素销售额将从 2018 年的人民币 8,700 万元增加至 2019/20 年的人民币 1.7 亿/2.4 亿元(高 于之前预测的 1.3 亿/1.8 亿元人民币)。 我们预计 2019/20 年盐酸美金刚的收入将为 7,500 万元/1.4 亿元人民币(略低于之前预测的 8,900 万元/1.51 亿元人民币),高于 2018 年的 人民币 4,400 万元,这有赖甘精胰岛素获纳入国家医保目录。

估值不高 我们审视了分类加总估值的假设(图二)。我们下调了各业务的估值(抗生素由 14 倍下调 至 10 倍,胰岛素估值倍数由 25 倍下调至 20 倍,而散装药和中间体产品由 8 倍下调至仅有 6 倍)。公司目前的 2019/20/21 年估值为 11.0/9.2/8.2 倍,考虑到 2018-2021 年每股盈利 约 13%的年复合增长率,股份估值不贵。催化因素包括:1)甘精胰岛素销售快速提升;2) 预计 2019 年末推出门冬胰岛素注射液;3)公司有机会出售成都的投资物业(账面值约 7 亿元人民币),这将为公司产生额外现金。

More Content

Physical Store(set to open in Q2 2025)

Address:

Shop LMC 307, 3/F, Lok Ma Chau MTR Station, Lok Ma Chau

Opening Hour:

9am - 9pm (Mon - Sat)

10am - 6pm (Sun and Public Holiday)

(set to open in Q2 2025)