本文來自格隆匯專欄: 梁中華宏觀研究 作者: 梁中華

·概 要 ·

中長期來看,我國經濟具有較大的增長潛力。不過短期來看,要鞏固經濟恢復的成果,還需要積極的穩增長政策進一步發力。10月24日,十四屆全國人大常委會第六次會議審議通過了國務院關於增加發行國債支持災後恢復重建和提升防災減災救災能力的議案,增發國債的規模達到1萬億元,反映了財政政策積極支持穩增長的態度。

在居民和企業需求還需要進一步提振的情況下,財政政策的發力有利於託底需求端。那麼要穩定經濟需求端,財政政策需要多大的規模呢?我們不妨做一些探討。

風險提示:假設和測算誤差風險;海外不確定因素髮酵。

從支出端來看,需要多少量?

要衡量財政的積極程度,可以看看財政支出總量的變化情況,這雖然是一種比較粗略的估計,但仍然可以提供一定的參考意義。截至今年9月份,我國公共財政支出和政府性基金支出合計累計同比增速為-2.4%,政府支出回落的最重要拖累因素是土地出讓收入的下降。一般來説,在經濟處於下行週期的時候,政府税收等收入端具有“順週期”的特性,也會同步下行,而財政政策如果要更好的發揮“逆週期”功能的話,則需要在收入端面臨壓力的時候,增加支出的強度。

如果按照(公共財政支出+政府性基金支出)/GDP衡量財政支出的強度,2019年這一比例為33.5%,2020年35.9%,2021年降至31.3%,2022年30.7%,截至2023年9月,海通證券估算這一比例年化為29.2%,比2019年低4個點附近。如果財政支出強度要回到2019年的水平的話,則意味着財政支出強度要提高4個百分點;如果財政支出強度回到2020年,則要提高6.7個百分點。

而這裏的支出強度還沒有考慮地方政府隱性債務擴張而增加的廣義財政支出。如果按照(公共財政支出+政府性基金支出+隱性債務增幅)/GDP衡量財政支出強度,2019年為38%,2020年43%,2021年回到36%,2022年36%,2023年考慮到預算收入和土地出讓收入下降,以及城投債務增速放緩,政府支出佔GDP的比例可能進一步下降。所以如果要彌補隱性債務擴張放緩帶來的支出減少,則財政支出需要增加的規模要大一些。

從赤字率來看:需要多少量?

不過,純粹用財政支出數據來衡量財政的力度,也會存在一定的偏差。例如,如果財政支出的擴張是通過大量加税帶來的,那直接用財政支出來衡量財政積極程度,則會存在一定的高估。所以可以用廣義財政支出減去廣義財政收入,算出廣義財政赤字率,用赤字的變化來衡量財政的力度。

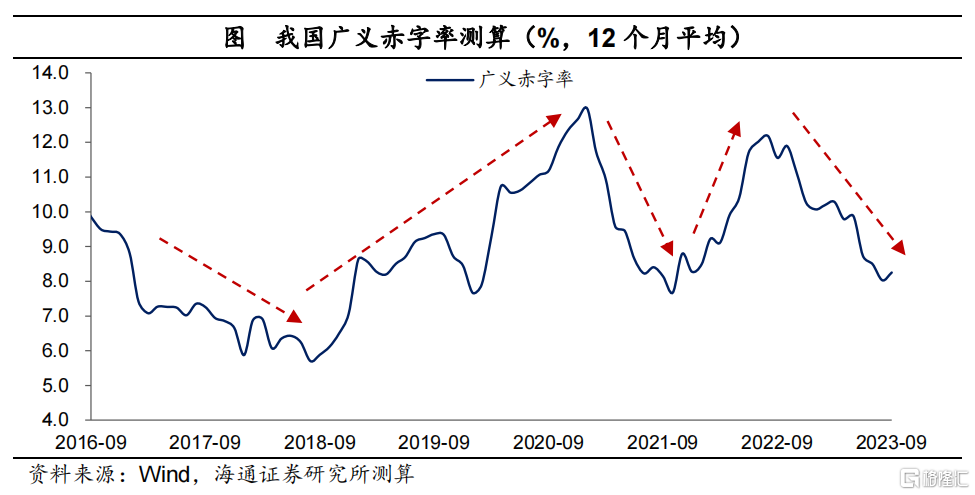

在測算廣義財政赤字率的時候,海通證券不僅考慮公共財政收支、政府性基金收支,還考慮了政策性金融債券淨融資、PSL融資、城投債券淨融資、鐵道債淨融資。截至今年9月份,連續12個月年化的廣義赤字率為8.3%,而2022年最高時為12.2%,2020年最高時為近13%。如果要回到2020年的財政強度,廣義赤字率要提高近5個百分點。

需要注意的是,海通證券這裏還沒有考慮地方隱性債務中貸款、非標等渠道擴張的放緩,如果考慮到這些,可能需要的赤字規模要更大一些。

政策的空間:很充足

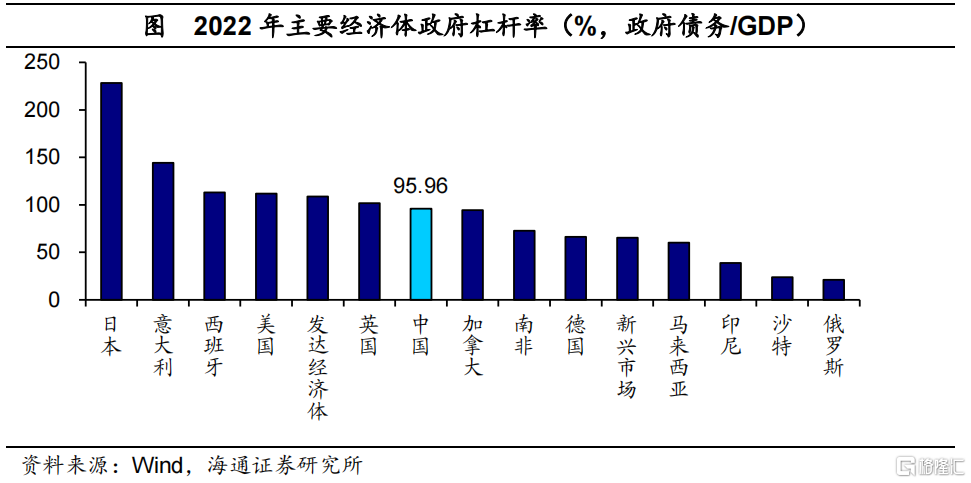

從政策的空間來看,我國財政政策的空間仍然是很充足的。根據海通證券的估算,即使把隱性債務規模考慮在內,我國的政府槓桿率雖然高於新興市場平均水平,但仍明顯低於發達經濟體政府槓桿率。同時,我國政府債務以本幣債務為主,我國具有通過政府債務的短期增加來穩定實體經濟需求端的實力。

如果能夠解決好央地財權、事權劃分的結構性問題,我國財政政策對實體經濟的支持空間就有希望釋放出來。去年底的中央經濟工作會議提出要防範化解地方政府債務風險,堅決遏制增量、化解存量;今年的中央金融工作會議指出,建立防範化解地方債務風險長效機制,建立同高質量發展相適應的政府債務管理機制,優化中央和地方政府債務結構。我國中央財政支出佔比較低,中央財政槓桿率也較低,是具有較大的政策空間的。在地方增量債務壓降的背景下,要保證“積極”的財政政策對經濟的支持力度,其他渠道的廣義財政增加支持,或是影響經濟恢復的重要觀察視角。

風險提示:假設和測算誤差風險;海外不確定因素髮酵。

注:本文來自海通證券於2023年11月6日發佈的《“積極”的財政:需要多少量?(海通宏觀 梁中華)》,分析師: 梁中華