本文來自格隆匯專欄:中金研究,作者:肖捷文、張文朗

上週公佈的美國9月零售銷售額環比增長0.7%,好於市場預期的0.3%,也是連續第六個月正增長。簡單扣除掉9月0.4%的CPI環比增速,實際零售環比增長仍有0.3%,年化後的增長率超過3%。

消費的強勁表現意味着美國經濟仍有韌性。本週四美國將公佈三季度GDP數據,根據亞特蘭大聯儲GDPNow模型的最新預測,Q3 GDP季調環比折年率有望達到5%,如果這個預測正確,那麼Q3實際GDP同比增速將達到3%,若加上3.5%的通脹,名義GDP同比增速或達6.5%,較Q2的6%進一步上升。

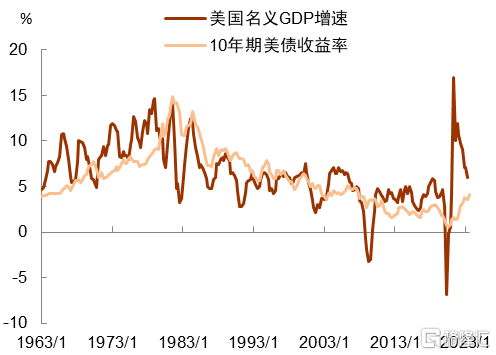

那麼,基於這些數據,美債利率5%的定價合理嗎?如果看2008年次貸危機後的十多年,美債利率從未達到5%,這似乎指向目前利率水平過高,不可持續。但如果看次貸危機前的1995-2005年,10年期美債收益率均值為5.3%,美國名義GDP同比增速均值5.4%,美債利率與名義GDP增長大致相當。如果以那段時間作為參考,那麼當前6%~6.5%的名義GDP增速或許應該對應6%以上的美債利率,而非5%(圖表1)。

圖表1:美債收益率上升受到基本面支撐

資料來源:Wind,中金公司研究部

那麼現在的問題是,以2008年前作為參考合適嗎?我們可以從兩個角度看:首先,從金融週期角度看,1995-2005年美國處於金融週期上行階段,2008年後金融週期轉為下行,直到2016年前後觸底,而後再次上行。也就是説,當前美國或仍然處於金融週期上行階段,這一點與2008年前的情況更相似。

其次,從宏觀政策角度看,金融週期下行階段,宏觀政策一般採取“緊信用、松貨幣”組合,為對沖信用收縮的負面影響,貨幣政策往往需要過度寬鬆,比如2008年後美聯儲實施了前瞻指引和量化寬鬆,加大了市場利率下行壓力。而在金融週期上行階段,由於信用擴張衝動更強,貨幣政策會傾向緊縮,以防止經濟過熱和通脹過高。新冠疫情後,供給衝擊一波接一波,通脹風險上升,這進一步增強了貨幣緊縮的必要性和持續性,加大市場利率上行壓力。

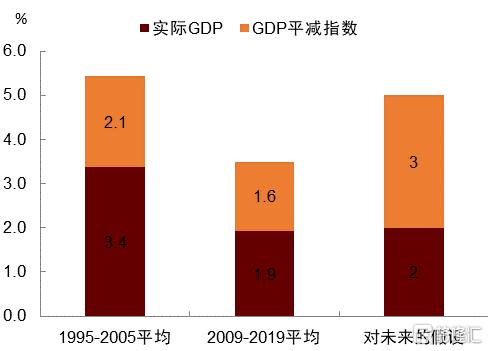

由此來看,當前的利率定價並沒有超越歷史,背後有基本面支撐。接下來的問題是,這樣的基本面是否可持續?我們不妨將當前6%的名義GDP增長拆分為實際GDP和通脹兩部分,大致來看,當前的實際GDP增長在2.5%左右,通脹在3.5%左右。考慮到美聯儲持續緊縮,貨幣金融條件收緊,未來經濟增長大概率放緩,但由於美國處於金融週期上半場,私人部門資產負債表健康,發生金融系統性風險的概率較低。我們不妨做一個假設,未來實際GDP增長中樞為2%,這並不是一個很強的假設,因為2009-2019年金融週期下行階段,實際GDP增長均值也有1.9%(圖表2)。該假設與美國國會預算辦公室(CBO)對未來十年美國實際GDP增長的假設也基本一致。

圖表2:對名義GDP增長率的分解

資料來源:美聯儲,美國國會預算辦公室(CBO),中金公司研究部

通脹方面,貨幣緊縮有利於抑制通脹,但由於近年來許多供給側因素髮生了深刻變革,長期通脹中樞或已抬升。我們一直有一個觀點:在人口老齡化、政府幹預經濟、地緣衝突頻發、逆全球化、綠色轉型的今天,不能低估供給衝擊長期化的風險。在百年未有之變局下,全球供給彈性下降,供應不確定、不穩定性上升,給定同等的需求,通脹的韌性將更強。從這個角度看,未來通脹中樞在3%左右是比較合理的,這其實也不是一個很強的假設,因為1995-2005年金融週期上行階段,全球化加速,生產效率大幅提升,通脹中樞也有2.1%。

這裏還有一個問題,就是供給衝擊是否會導致美國經濟增速下降?我們認為可能會有一定影響,但這種影響可以部分被金融週期上行帶來的總需求擴張所彌補。也就是説,未來幾年美國的宏觀環境或將是與疫情前相當的經濟增長和比疫情前更高的通貨膨脹。這給美聯儲貨幣政策帶來了一個重要含義,那就是如果想維持之前的經濟增長,大概率需要提高通脹容忍度。

最後,我們把經濟增長率和通脹相加,大致得出名義GDP增長中樞在5%左右,簡單參考歷史經驗,這意味着5%的長期美債利率或是一種新常態。我們認為,這種新常態並非脱離基本面的存在,而是金融中週期波動,疊加供給側結構性變化帶來的結果,也是全球政治、經濟、社會發展到這個階段的規律。但這也不是説美國利率就一直處於5%,而是説圍繞5%波動的時間會更久,未來我們或更難回到疫情前的低利率時代。

注:本文來自中金公司2023年10月22日已經發布的《 5%的美債利率合理嗎?》,報吿分析師:肖捷文 S0080523060021,張文朗 S0080520080009