以史爲鑑,美聯儲轉向伴隨哪些前瞻信號?哪個階段交易勝率更高?

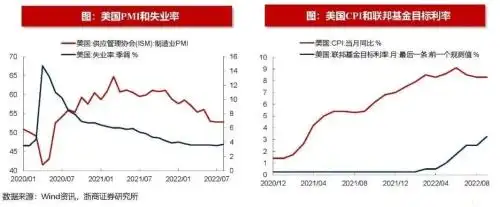

機構指出,從歷史來看,美聯儲貨幣政策轉向可以通過觀察PMI是否快速下降逼近榮枯線爲前瞻信號,美國經濟在加息週期的後期往往容易出現衰退的跡象。

來源:王楊策略研究

另外,市場表現最好的階段爲加息轉降息期間,其次爲初次降息後3個月,表現相對較差的是加息結束前3個月。

2022年傑克遜霍爾會議上美聯儲主席鮑威爾發表「鷹派」發言,重申美聯儲加息的決心。隨後9月美聯儲議息會議上,美聯儲加息75bp。全球股市在連續加息的壓力下,波動明顯加大,當前美聯儲政策拐點成爲市場關注焦點。

美國從80年代以來一共經歷了六輪完整的加息週期,分別是1982年12月-1984年8月,1987年1月-1989年5月,1994年2月-1995年2月,1999年6月-2000年5月,2004年6月-2006年6月,2015年12月-2018年12月。

根據歷史六輪美聯儲加息轉降息的覆盤經驗,貨幣政策轉向可以通過觀察PMI是否快速下降逼近榮枯線爲前瞻信號,美國經濟在加息週期的後期往往容易出現衰退的跡象。

歷史上,美聯儲尚未在聯邦基金利率低於CPI期間進行降息。目前聯邦基金目標利率爲3.25%,美國CPI和核心CPI分別爲8.3%和6.3%,聯邦基金目標利率距離通脹仍有較大的距離。

從1980年以來六輪美聯儲加息轉降息階段的市場表現來看,市場表現最好的階段爲加息轉降息期間,其次爲初次降息後3個月,表現相對較差的是加息結束前3個月。邏輯上來看,最後一次加息後,經濟衰退跡象顯現,市場預期貨幣政策從緊轉鬆,資本市場往往會提前開啓上漲行情。

哪些行業有望脫穎而出?

統計每輪核心上漲階段的行業表現,漲幅居前行業多爲金融(第一/二/六輪)、資源(第一/三/五/六輪)、電子(第三/五/六輪),與此同時,消費中的耐用消費品和日用消費品往往漲幅排名居後。

邏輯上,金融爲早週期受益邏輯,電子則受益於流動性的寬鬆,資源在加息結束前多表現爲下跌,但隨着降息的臨近,市場對經濟預期開始改善,繼而帶動資源股股價上漲。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of this article is for reference only. It does not constitute an offer, solicitation, recommendation, opinion or guarantee of any securities, financial products or instruments.The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance.