美元站上114之後

本文來自格隆匯專欄:興證宏觀王涵,作者:卓泓、彭華瑩、王涵

9月聯儲會議後海外市場劇烈,波動呈現是除了美元其他資產幾乎全被拋售的格局:美元一度衝破114,10Y美債利率衝破3.8%,美股基本抹平6月反彈以來所有漲幅,黃金和大宗也全面回調。對此我們認爲:

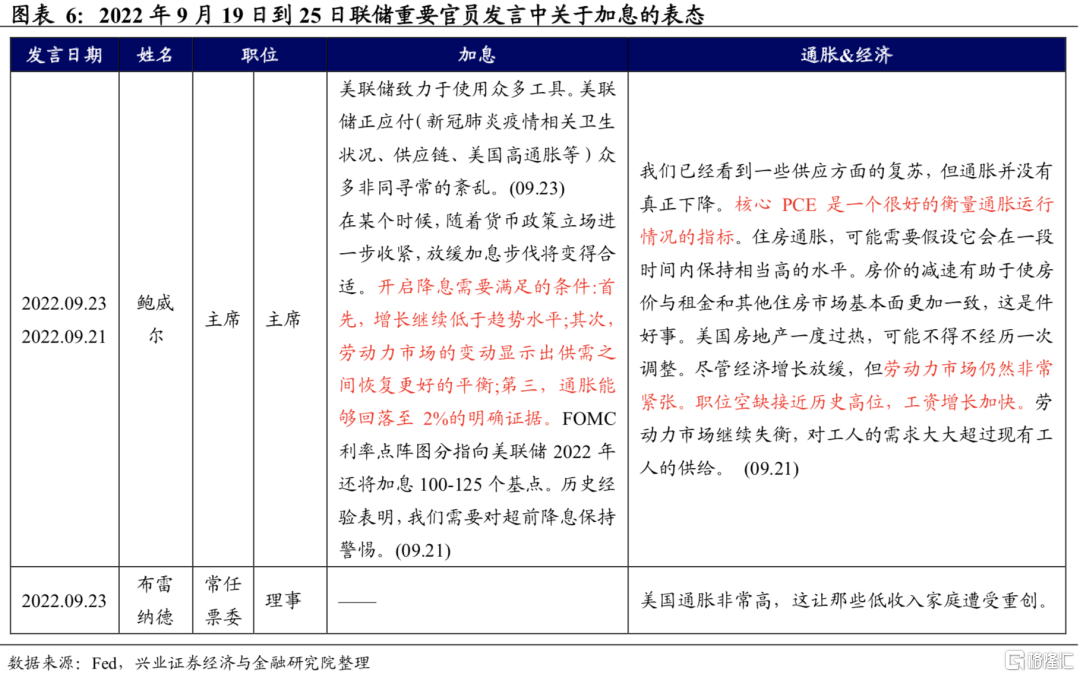

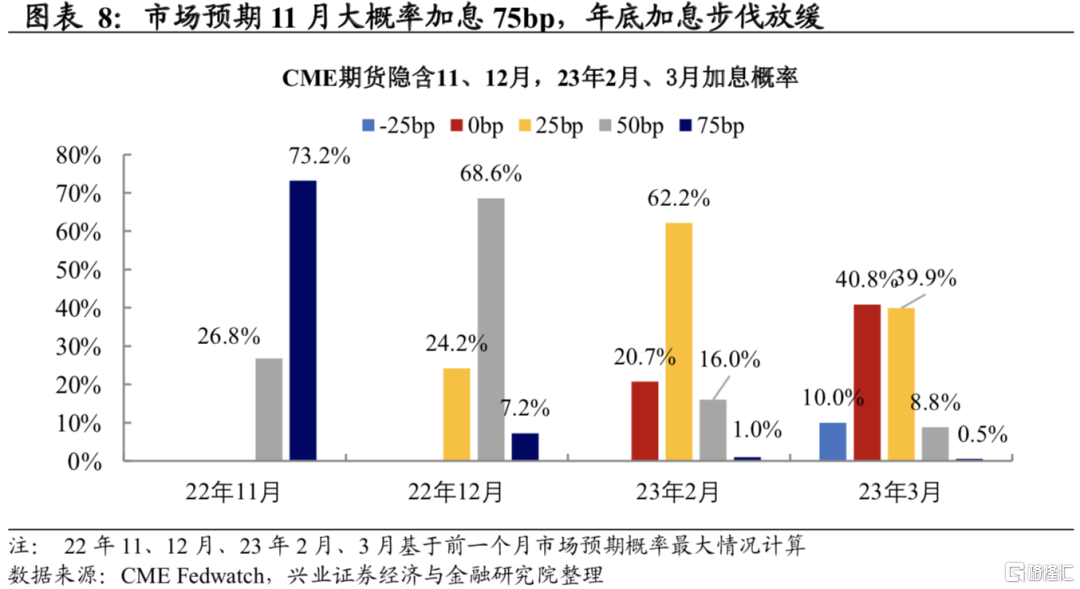

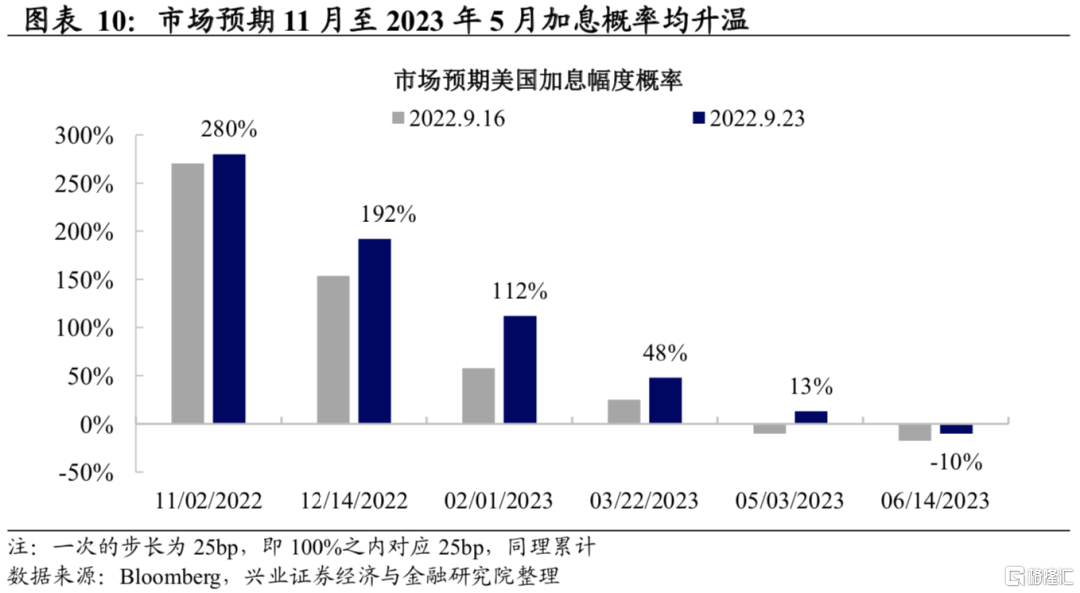

市場核心仍然在擔憂央行各國央行更陡峭的緊縮導致的衰退。儘管此前市場充分預期9月加息75bp,但關鍵在加息的終點:相較於會前市場預期的加息終點4%,點陣圖顯示多數官員本輪加息終點將升至4.5%至5%。節奏來看,市場預期11月加息75bp、12月加息50bp、23年2月加息25bp,而後開始放緩加息的步伐。會後聯儲主席Powell和官員Brainard繼續放鷹,最新公佈的9月Markit PMI也強於預期,更加支撐聯儲的緊縮。

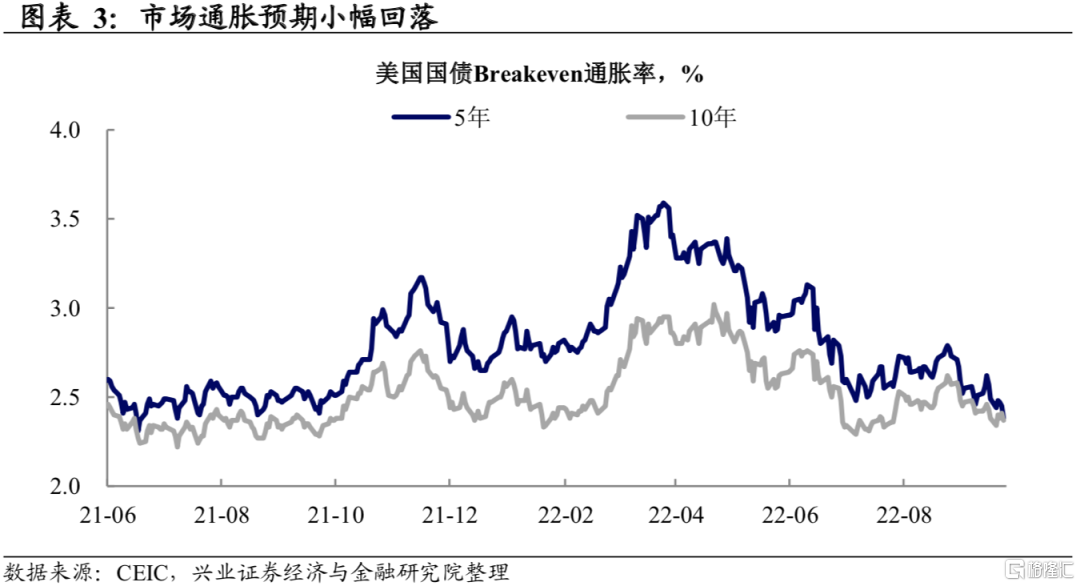

美國通脹粘性的核心矛盾是勞動力短缺。供給層面,油價持續回落,供應鏈也持續改善(美國洛杉磯和長灘港在泊位及外圍等待的船隻數回落至歷史低位)。但核心在勞動力供給:我們在9月9日報告《就業纔是關鍵》討論過,超額儲蓄支撐下的低端勞動力預期將繼續迴歸,但新冠導致的階段性供應短缺可能致使勞動參與率缺口難以閉合,進而使工資回落緩慢。更爲陡峭的菲利普斯曲線也意味着抗通脹需要更大的犧牲:市場衰退預期愈演愈烈,10Y-2Y利差進一步加大至51bp,創2000年4月以來新高。

央行“摸着石頭過河”,美元強勢及美股美債震盪可能處於黎明前的黑暗。雖然央行緊縮只能影響需求端,但爲了通脹預期的錨定,貨幣政策只能選擇更加陡峭的路徑,而由於供給改善速度難以預測,各國央行只能“摸着石頭過河”,緊縮超調依然存在。在這種尾部階段,股債可能都仍將盡力震盪。11月FOMC會議前,關注10月7日的非農數據和10月13日的美國CPI數據。除了聯儲的鷹派,德國PMI的弱勢、英國“緊貨幣+寬財政”的組合引起的市場對其債務和通脹的擔憂,都有望助推美國在未來一段時間內相較於非美經濟體維持強勢,美元預期也將繼續維持強勢。

匯率壓力暫時仍然存在,但不改貨幣政策以我爲主的空間。美元強勢預期將繼續給人民幣帶來貶值壓力。但是,今年以來美元指數連續走強的過程中,人民幣貶值是階梯式、脈衝式的:除了4月的急貶和8月中以來的回調,其餘時間人民幣相對於美元是不弱的。這說明,相對於利差,疫情防控前景和經濟增長前景等內生驅動力可能在今年人民幣匯率走勢中扮演了更重要的角色。基於此,穩增長訴求下,貨幣政策以我爲主的邏輯依然存在。

風險提示:通脹持續性超預期,聯儲貨幣政策收緊超預期。

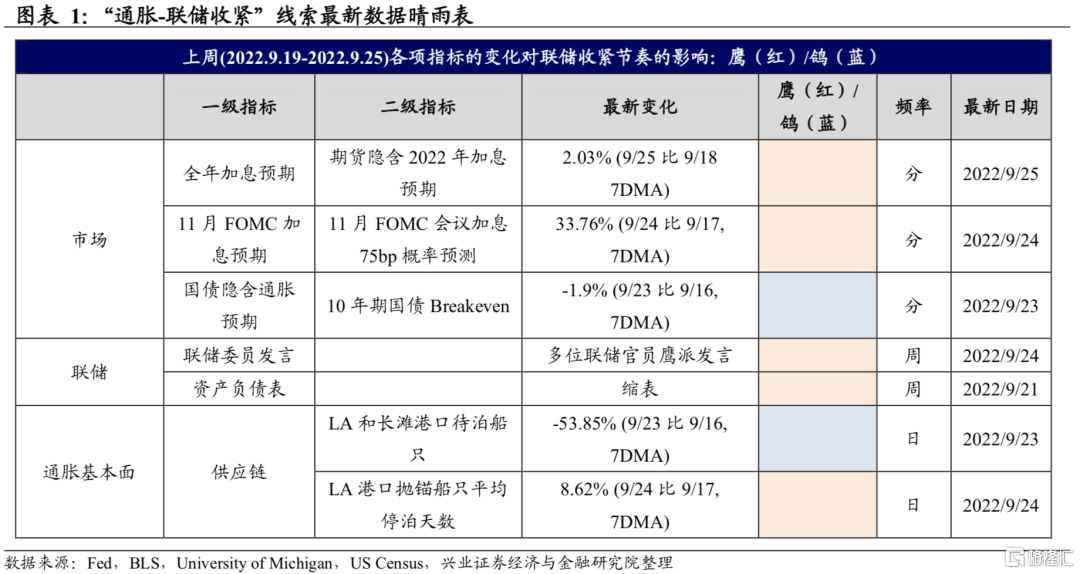

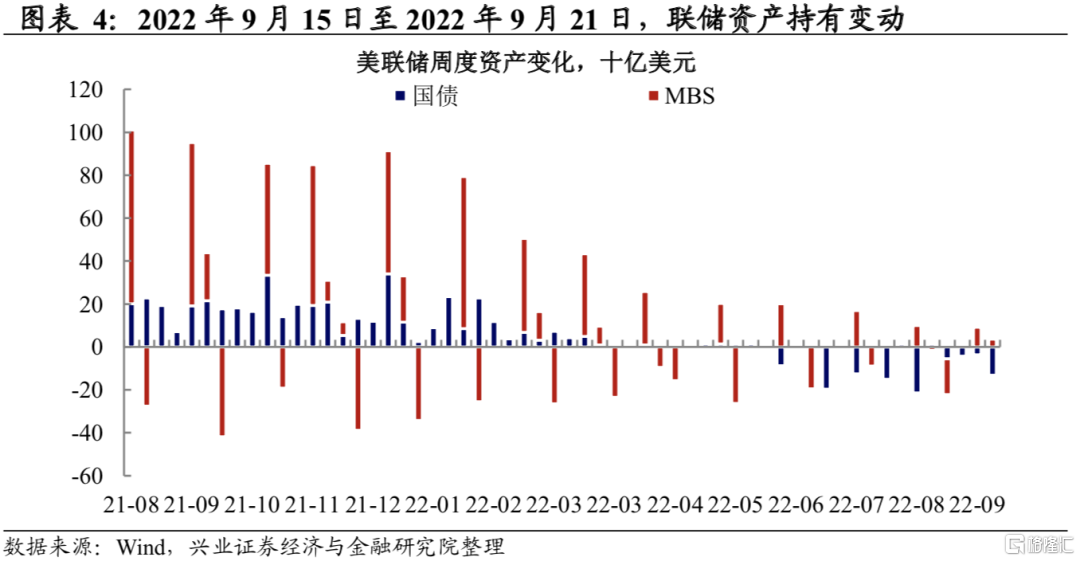

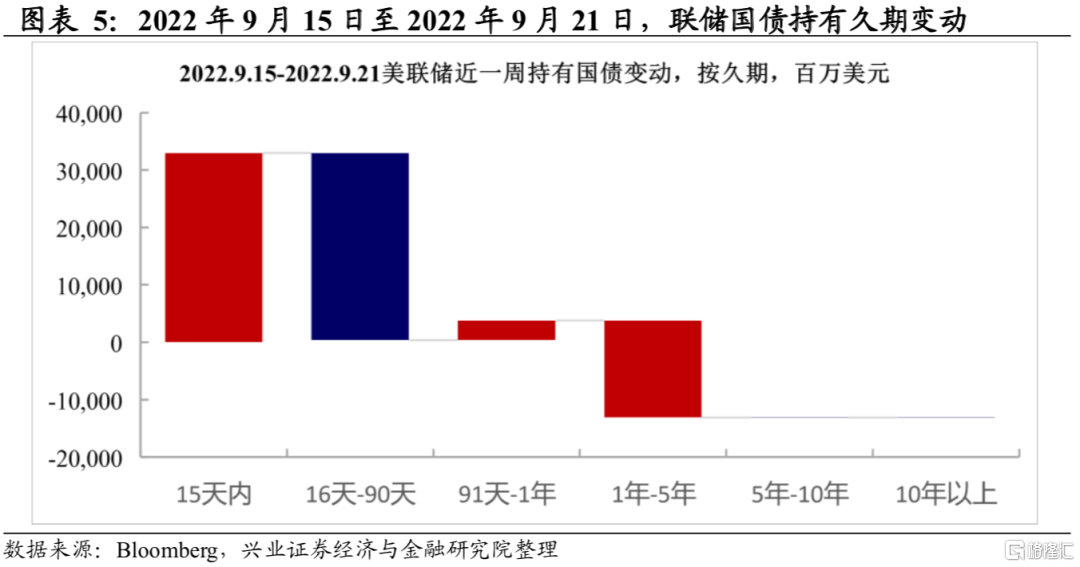

“通脹-聯儲收緊”線索追蹤

市場:聯儲鷹派態度堅定,

加息幅度預期上升

通脹:供應鏈壓力整體緩和

風險提示:通脹持續性超預期,聯儲貨幣政策收緊超預期

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of this article is for reference only. It does not constitute an offer, solicitation, recommendation, opinion or guarantee of any securities, financial products or instruments.The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance.