本文來自格隆匯專欄:陶川

2022年3月,挪威主權基金GPFG剔除李寧的事件為市場敲響了警鐘,引發市場對於未來此類事件發生頻率增加的擔憂。導火索便是ESG投資中被廣泛使用的負面篩選策略,在此策略下,投資機構通常會制定排除政策,建立負面清單,而李寧正是被列入了GPFG的負面清單。

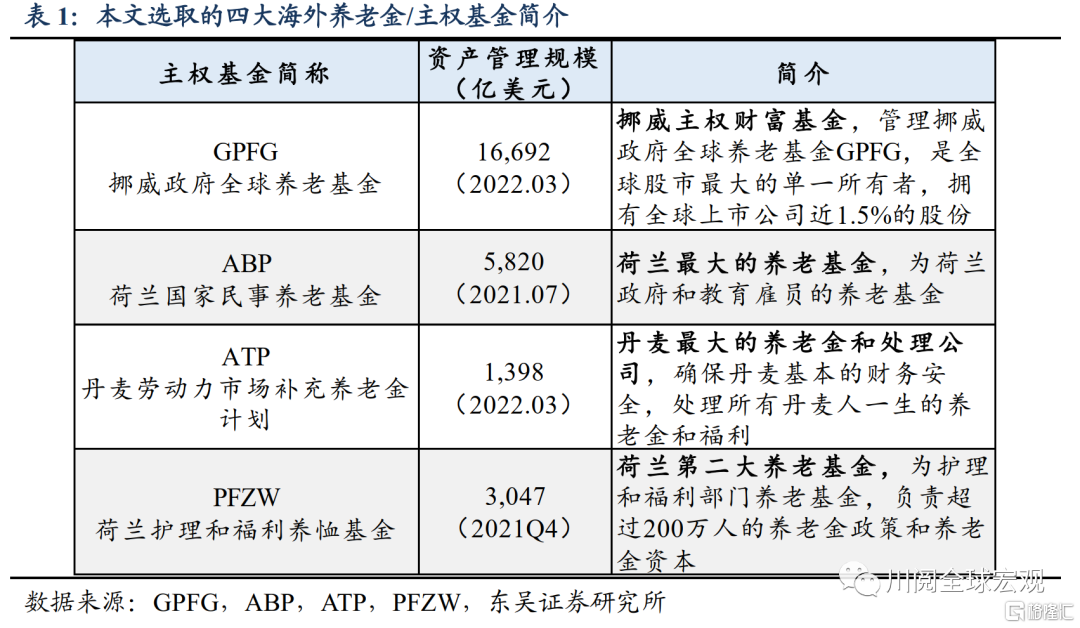

本文從風險管理的角度,對海外養老金及主權基金的負面清單進行了研究。我們選取了資產管理規模較大、在ESG投資方面領先的四大海外養老金/主權基金作為研究對象,對其負面清單上的公司進行了分析(表1)。

上述四家機構分別為挪威主權基金GPFG、荷蘭公共部門養老金ABP、丹麥勞動力市場補充養老基金ATP以及荷蘭衞生保健基金PFZW。它們的資產管理規模合計超2萬億美元,投資範圍共計排除了全球近400家公司。我們對登上負面清單的公司進行了以下三點概括:

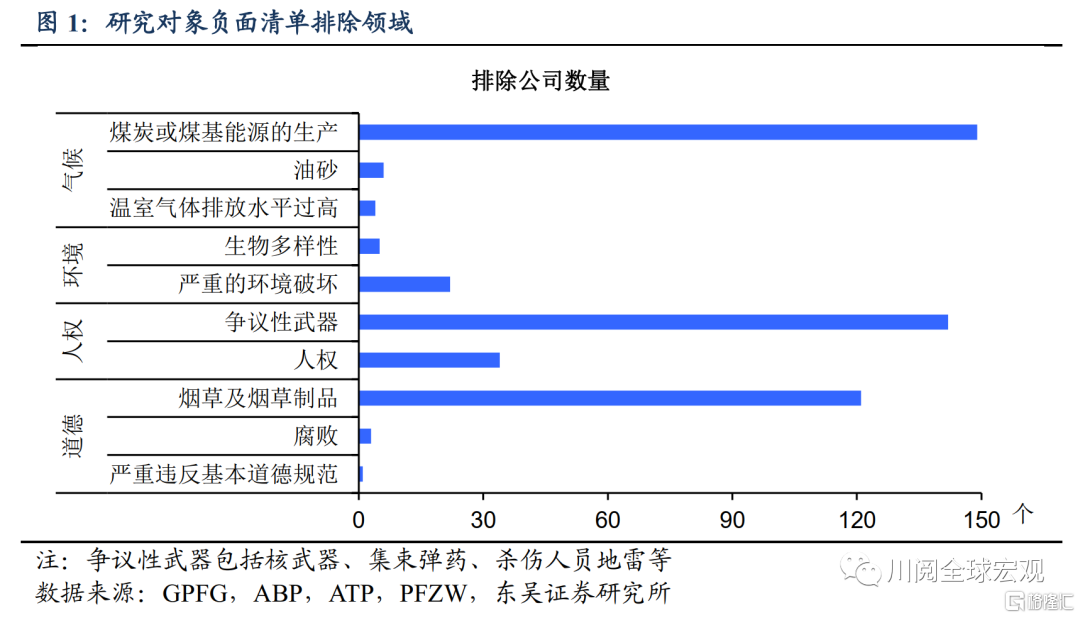

一是領域方面,主要分佈在氣候和環境、人權、道德三大領域,佔比分別為38%、36%、26%(圖1)。被排除公司的分佈集中度較高,在共計10個細分領域中,排除公司數量Top3的領域就佔了85%,分別為煤炭或煤基能源的生產(佔比31%)、爭議性武器(29%)和煙草及煙草製品(25%)。

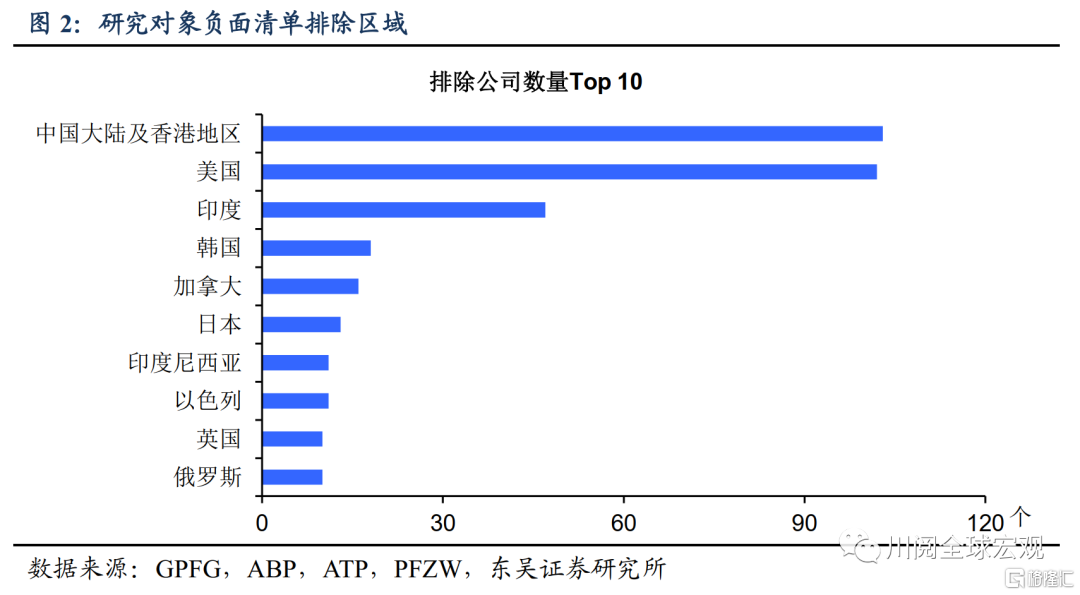

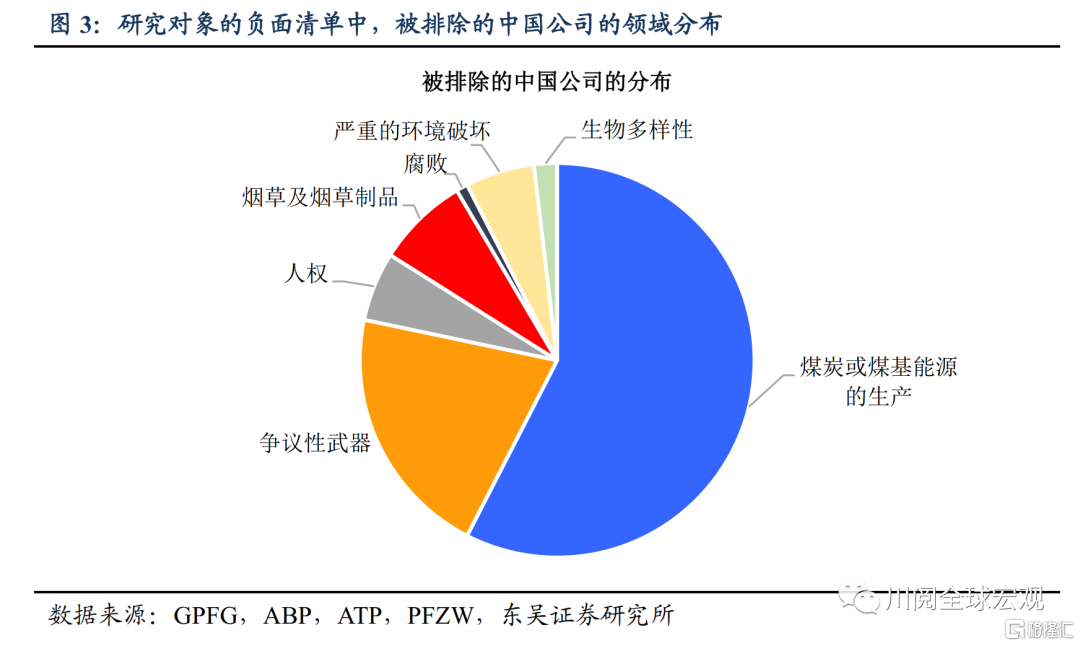

二是地區方面,僅中美兩國的佔比便高達42%(圖2)。當然主要原因也在於中美資本市場規模巨大,其被投資公司的基數也大。被排除公司數量位居前五的國家還包括印度(佔比10%)、韓國(4%)、加拿大(3%)。從細分領域看,對於被排除的中國公司,比較反直覺的發現是,多數公司業務在煤炭或煤基能源的生產領域(佔比被排除的中國公司的58%),而常被西方媒體渲染的人權領域佔比不足6%(圖3)。

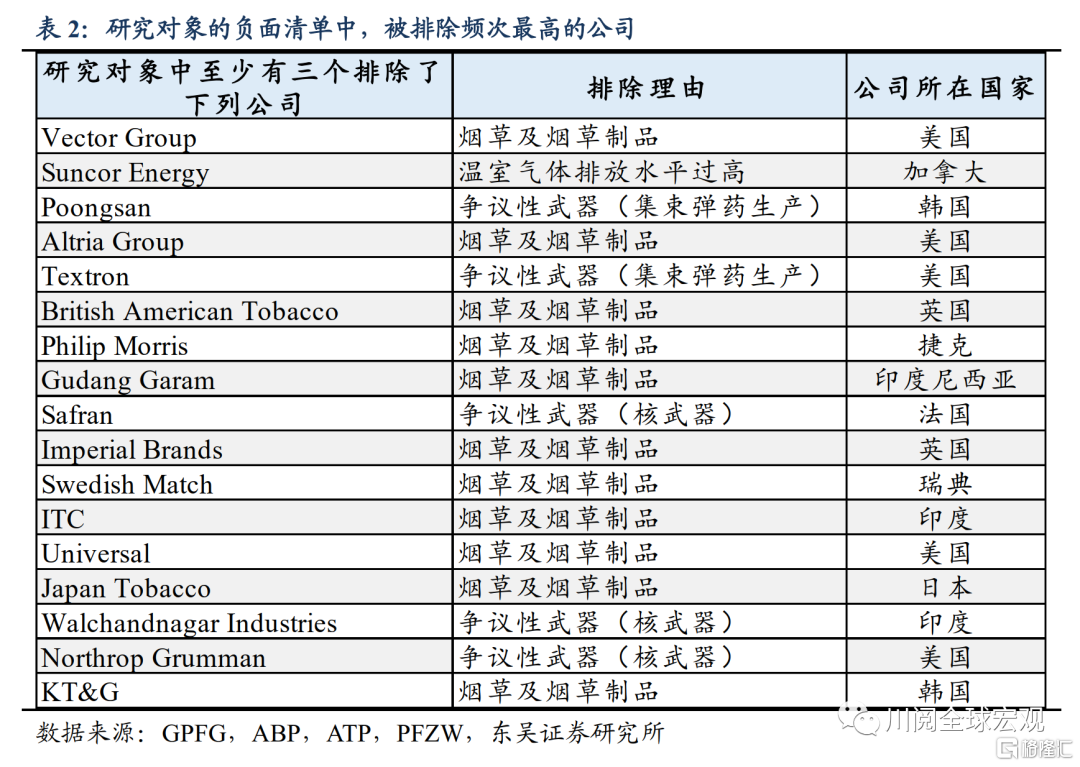

三是公司層面,被排除頻次最高的多為煙草及煙草製品公司(表2)。被我們4個研究對象中至少3個排除的公司共計17個,其中11個被排除的原因為涉及煙草領域的業務。

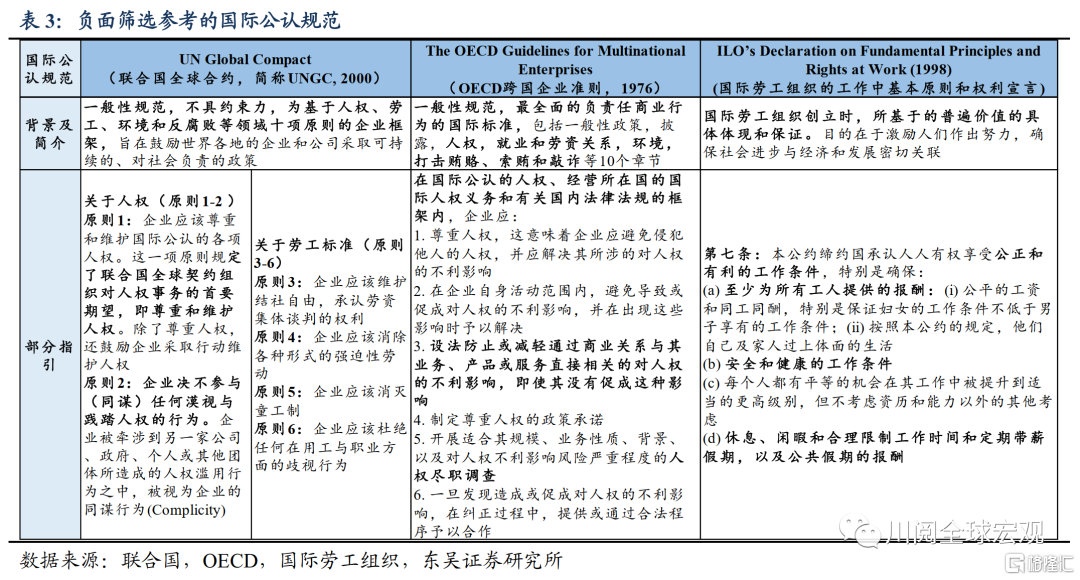

那麼,海外機構的排除標準(或者説是負面篩選標準)是如何確定的?參考國際公認規範,並且依據機構所在國自身法律的要求。

我們此前的報吿《新趨勢下的投資避險指南——ESG系列研究開篇》指出,負面篩選基於傳統道德價值觀及標準和規範,規避公司或國家。價值觀聚焦公司業務,例如上述對煙草領域公司的排除,通常採用限定財務閾值(如負面業務佔比總收入)。標準和規範聚焦公司在人權、勞工、環保等領域國際公認規範方面的行為。

如表3所示,國際上公認的一般性規範包括UNGC(聯合國全球合約)和OECD跨國企業準則;勞工權利(人權細分項)參考的規範包括國際勞工組織的工作中基本原則和權利宣言;爭議性武器方面的國際規範包括渥太華條約、集束彈藥公約、化學武器公約、生物武器公約、核不擴散條約等,而具體到國家層面,例如荷蘭2013年修訂了其金融監管法的市場濫用法令,納入了荷蘭金融機構在集束彈藥方面融資方面的義務(對其融資等方面的限制)。

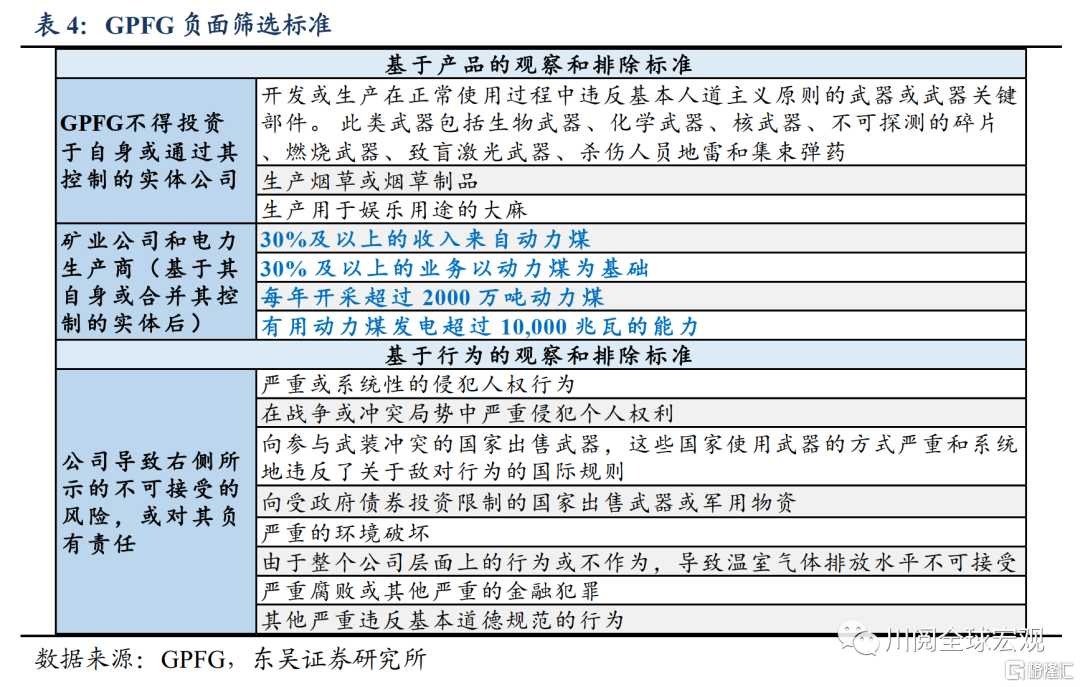

GPFG的負面篩選標準極具代表性。其參考的國際規範主要包括UNGC、 OECD跨國企業準則、G20/OECD公司治理原則、聯合國貿易和發展會議的促進負責任主權借貸原則。其排除標準分為兩種,分別基於產品和行為(表4),比較典型的是其對於礦業公司和電力生產商的排除,採用了設立閾值的方式,在動力煤方面對於收入佔比、業務領域佔比、開採量、發電能力等方面設立了門檻,排除超過門檻限定的標的公司。

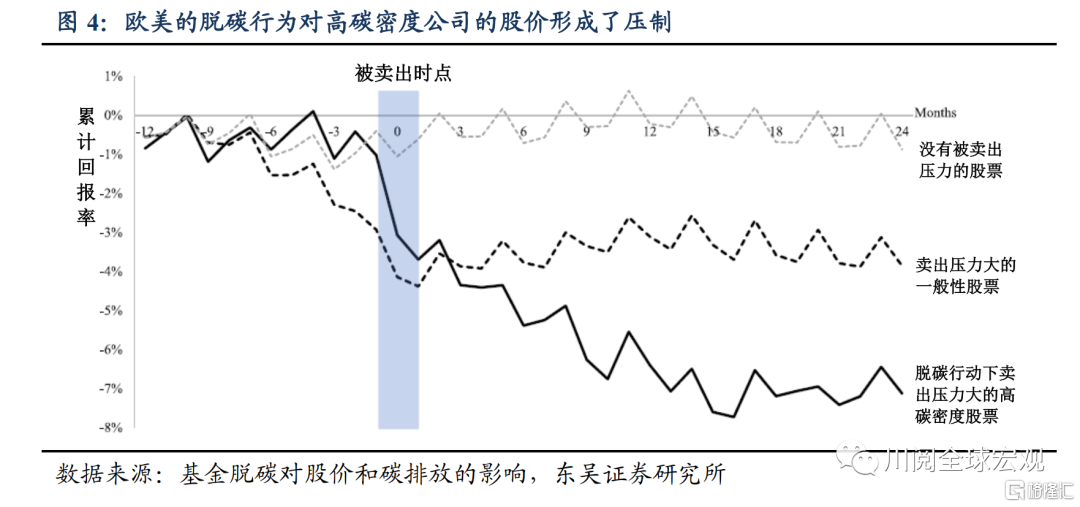

基金剔除壓力對於標的股價的影響有多大?

2010-2017年間,歐美的脱碳行為對高碳密度公司的股價形成了壓制。德國奧格斯堡大學的研究對歐洲和美國基金在2010-2017年間的脱碳行為進行了分析,結果表明在被賣出時點,那些由於基金脱碳行為而面臨高賣出壓力的高碳密度股票,其股價的跌幅近3%,並且鑑於脱碳行動的持續性,對於上述類型股票的負面影響持續了兩年之久(圖4)。

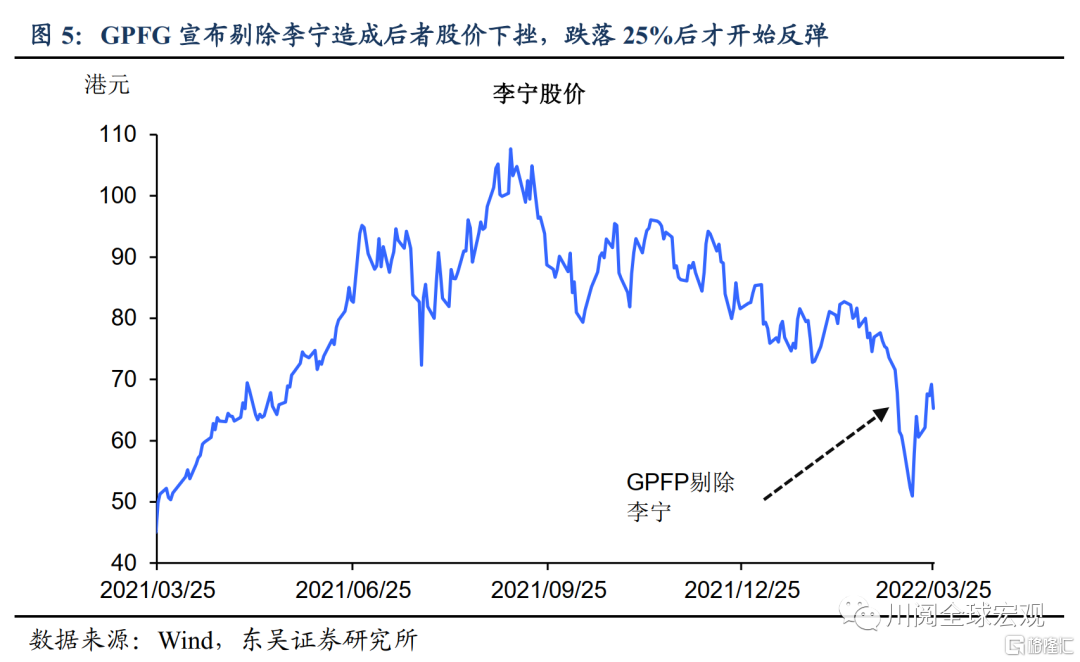

此外,短期內的影響不容易小覷,當涉及投資規模較大的大型機構時對市場的影響尤其顯著。2022年3月9日,GPFG將李寧納入負面清單,至3月15日累計跌幅達25%後觸底反彈,3月25日基本修復至宣佈撤資前的水平(圖5)。

儘管存在李寧等先例,但總體來看,大型海外機構出於意識形態差異而剔除我國股票的行為尚未形成顯著規模。一方面,當前海外機構的排除清單仍聚焦能源、爭議性武器和煙草領域;另一方面,對於我國股票的排除大多集中在氣候領域,除爭議性武器外的人權領域佔比較低,趨勢性的轉變尚未發生。因此,我們認為年內由於大型海外機構的排除政策而導致我國市場劇烈波動的風險不大。

風險提示:地緣衝突劇烈導致全球碳中和趨勢被逆轉;新冠病毒變異導致疫苗失效,造成資產價格崩盤

More Content

Physical Store(set to open in Q2 2025)

Address:

Shop LMC 307, 3/F, Lok Ma Chau MTR Station, Lok Ma Chau

Opening Hour:

9am - 9pm (Mon - Sat)

10am - 6pm (Sun and Public Holiday)

(set to open in Q2 2025)