據上交所消息,江蘇菲沃泰納米科技股份有限公司(以下簡稱“菲沃泰”)於3月18日首發上會,菲沃泰擬在科創板上市,中金公司為其保薦人。

公司本次擬募資16.64億元,其中8.31億元用於總部園區項目、3.33億元用於深圳產業園區建設項目以及5億元用於補充流動資金。

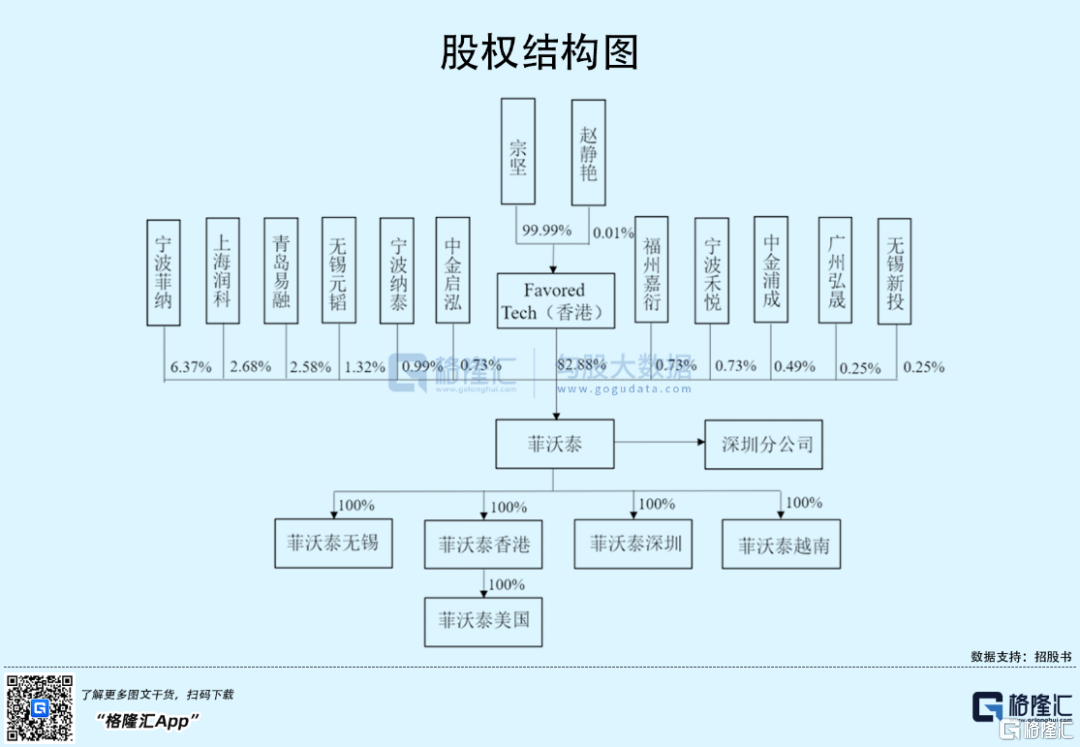

截至發行前,菲沃泰的控股股東為Favored Tech(香港),實際控制人為宗堅、趙靜豔,二人通過Favored Tech(香港)合計控制公司82.88%的表決權。

1

綜合毛利率波動下降

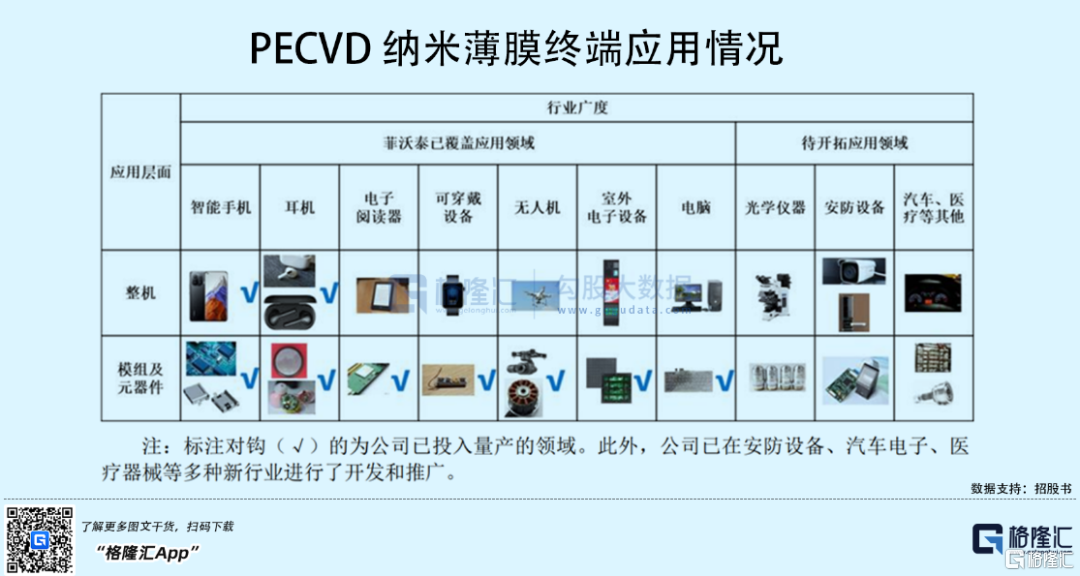

菲沃泰主要從事納米薄膜的研發和製備,併為客户提供納米薄膜產品及配套的鍍膜服務以及銷售納米鍍膜設備。

納米薄膜材料目前已經廣泛應用在智能手機、耳機、電子閲讀器、可穿戴設備、無人機等電子消費品領域。

近年來,由於下游智能手機廠商快速發展,尤其是華為、小米等公司的智能手機出貨量穩步提升,使得菲沃泰的收入規模也隨之增長。2018年至2020各報吿期,菲沃泰實現營業收入分別為6991.02萬元、1.43億元、2.38億元和2.31億元,淨利潤分別為1494.71萬元、3168.57萬元、5555.00萬元和1586.69萬元。

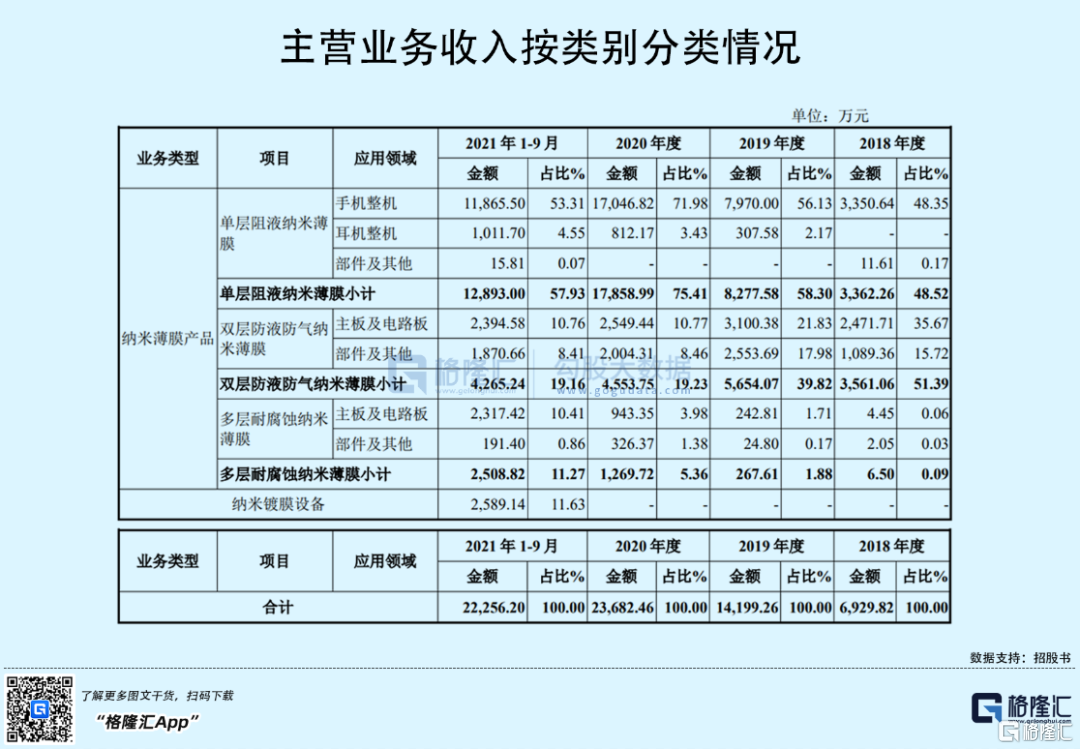

目前公司的納米薄膜產品系列包括單層阻液納米薄膜、雙層防液防氣納米薄膜和多層耐腐蝕納米薄膜,其中,單層阻液納米薄膜收入佔比最高,各報吿期佔主營業務收入比例分別為48.52%、58.30%、75.41%和57.93%,呈現先升後降的趨勢。

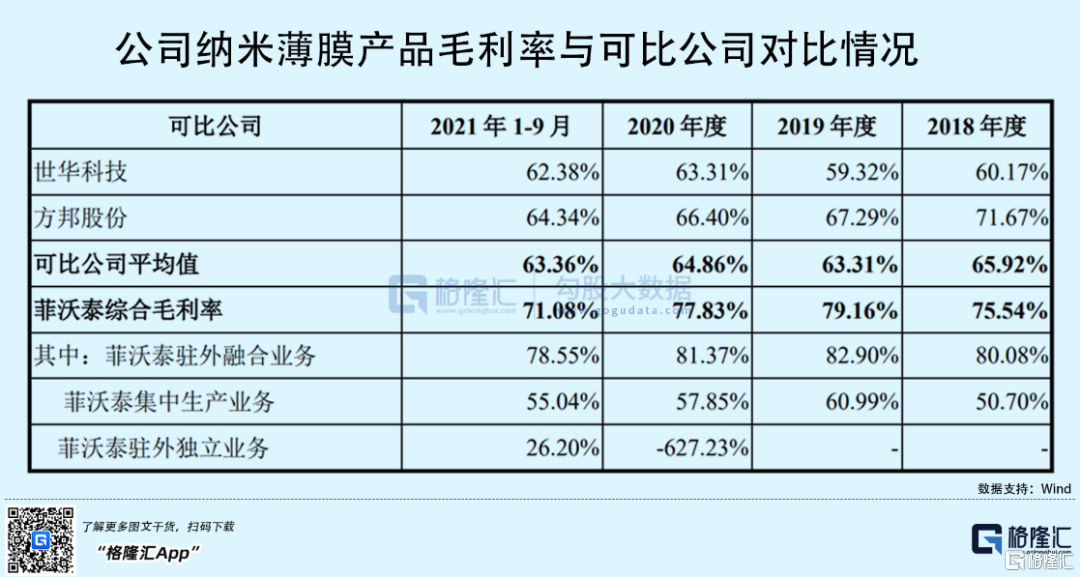

毛利率方面,近年來菲沃泰的綜合毛利率一直處於較高水平,報吿期內分別為75.54%、79.16%、77.83%和69.46%,雖高於可比公司平均水平,但2020年已呈現下降趨勢。

按生產模式來看,菲沃泰納米薄膜產品的主要生產模式是駐外生產模式,具體包括駐外融合生產模式和駐外獨立生產模式。

駐外獨立生產模式固定成本較高,目前主要是蘋果公司耳機類項目採用此模式;而駐外融合生產模式是採用融合模式下襬盤及上下料等工序的操作人員、場地、電力均由客户提供。報吿期各期,公司的駐外生產模式收入佔納米薄膜產品收入的比例均超過八成,佔比較高。

由於駐外融合生產模式生產同種產品所發生的成本較低,因此該業務毛利率較高。報吿期內,公司駐外融合生產業務毛利率分別為80.08%、82.90%、81.37%和78.55%。

值得注意的是,自2020年第三季度起,受芯片供應短缺的影響,華為、小米、歌爾股份等駐外融合生產模式的主要客户智能手機出貨量均有所下降,以致2021年1-9月菲沃泰的駐外融合生產業務收入有所下滑。未來若公司毛利率較高的駐外融合生產業務收入佔比持續下降,則公司的綜合毛利率可能會被拉低。

2

依賴前五大客户

目前菲沃泰與全球頭部科技企業建立了一定程度的合作關係。其中,公司與小米、華為的合作主要是為其手機整機、主板及電路板鍍膜;與蘋果的合作方式主要是通過蘋果的EMS廠商立訊精密和歌爾股份,為蘋果耳機類產品製備的納米薄膜產品量產。

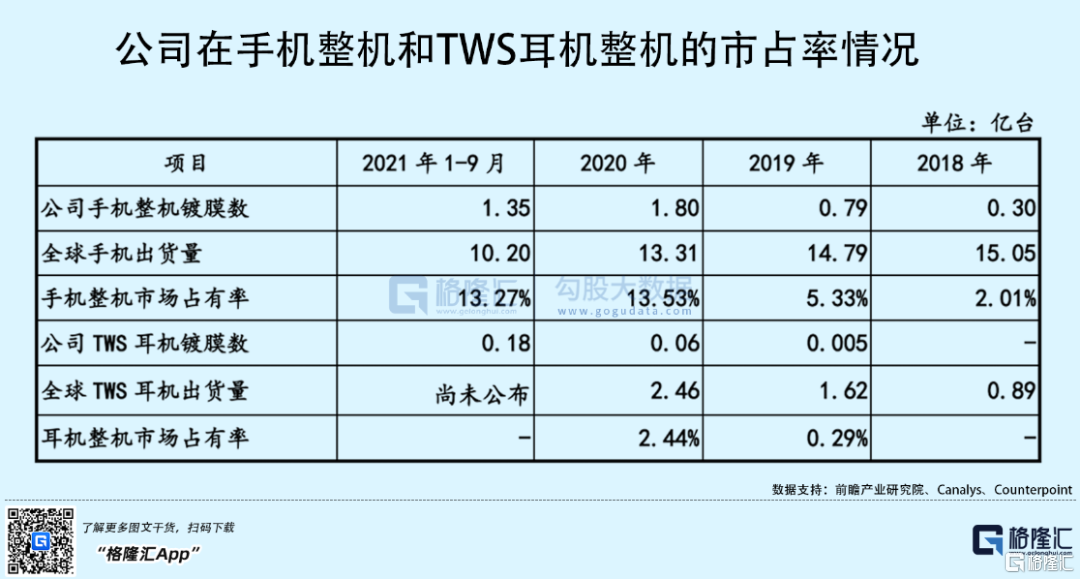

在菲沃泰的主營業務中,手機整機領域收入佔比較高。報吿期各期,公司在手機整機市場市佔率分別為2.01%、5.33%、13.53%和13.27%。

公開資料顯示,公司在華為手機整機鍍膜中的滲透率從2018年的9.80%提升到2021年1-9月的52.52%;在小米手機整機鍍膜中的滲透率從2018年的6.41%提升到2021年1-9月的75.62%。

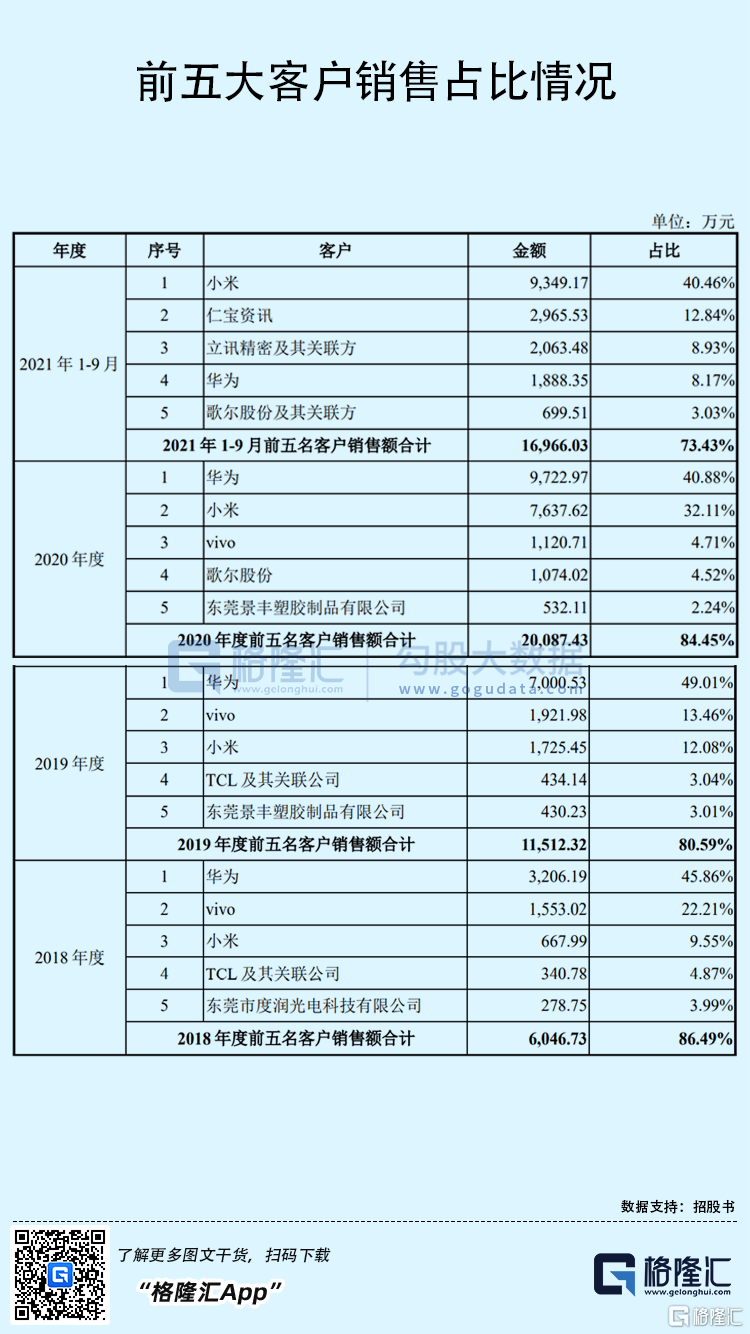

報吿期各期,菲沃泰來自前五大客户的銷售收入佔當期營業收入的比重分別為86.49%、80.59%、84.45%和 73.43%,主要客户為小米、立訊精密、仁寶資訊、華為和維沃等,公司存在一定的客户集中度較高的風險。

隨着菲沃泰在華為、小米手機整機鍍膜業務的滲透率進一步提升,公司對大客户的依賴程度也進一步加大。2021年前三季度,公司來源於華為的銷售收入為1888.35萬元,同比下降76.58%;2020年和2021年前三季度,來源於維沃的銷售收入分別為1120.71萬元和610.73萬元,同比下降41.69%和38.64%,同期,公司的主營業務收入及毛利率均受到不同程度的影響。

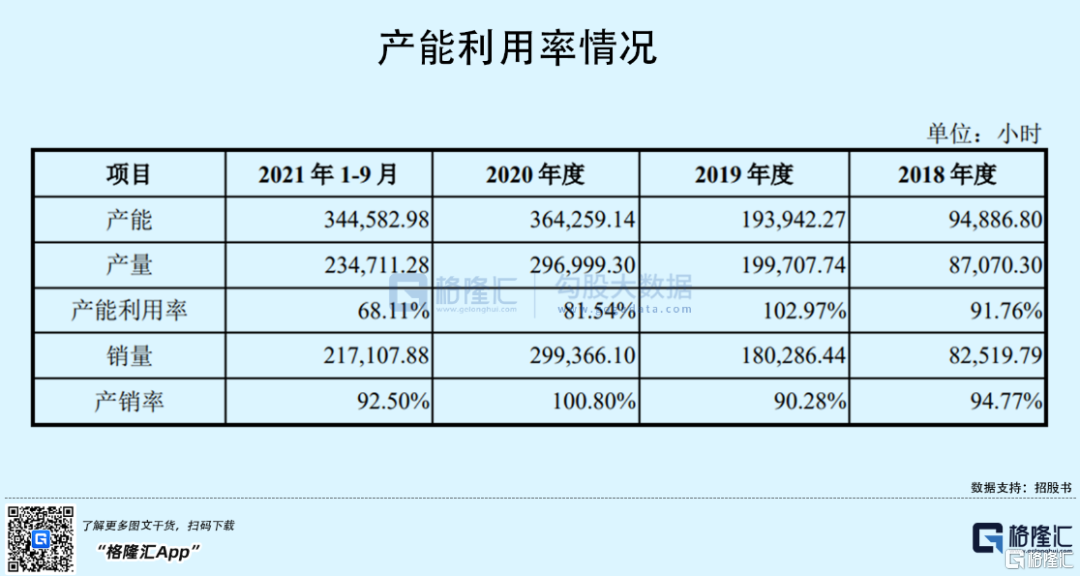

另外,受華為、維沃等客户部分機型減產的影響,2020年菲沃泰的產能利用率有所下降,報吿期各期,公司的產能利用率分別為91.76%、102.97%、81.54%和68.11%。

3

結語

整體來看,受益於下游消費電子板塊的快速發展,菲沃泰的營收規模有所增長,公司毛利率也保持較高水平,但公司過於依賴大客户的訂單,容易受到客户減產或行業價格戰的影響。目前下游消費電子行業客户對PECVD納米薄膜防護技術的功能、性能等需求不斷升級,市場競爭較為激烈。未來,公司仍需進一步加大研發,在保持產品市場競爭力的基礎上,積極開拓新的客户和渠道。

More Content

Physical Store

Address:

Shop LMC 307, 3/F, Lok Ma Chau MTR Station, Lok Ma Chau

Opening Hour:

9am - 9pm (Mon - Sat)

10am - 6pm (Sun and Public Holiday)