洪灝|央媽闡明貨幣政策立場

央行昨日(1月18日)在新聞發佈會上清晰地解讀了其貨幣政策。當前,“靠前”的寬鬆政策以防止“信貸塌方”,以及“精準”地瞄準最需要幫助的經濟部門以提供“充足”的流動性支持。市場共識聞風而動。

可以理解,共識期待今年市場開局疲弱後能有所反彈。但在尚未看到有力的市場證據之前,我們不會如共識一般倉促地妄下結論。

許多人將最近的雙降解讀爲一項“拯救”房地產行業的舉措。但在2018年初“房住不炒”的政策宗旨宣佈後不久,房地產行業的相對錶現就已經觸頂。同時,儘管2020年初新冠疫情爆發後出臺了積極的寬鬆政策,但房地產行業的相對錶現卻每況愈下,直到2021年7月達到一個短週期性底部(圖表1)。

因此,房地產行業的長期相對錶現反映了消除阻礙中國未來增長的“三座大山”的戰略規劃。而從短期來看,房地產行業其實一直對本輪貨幣寬鬆翹首以盼。事實上,中國房地產指數最近已經觸及一年來的高點——這與充斥在新聞頭條中慘淡的言論形成了鮮明對比。

圖表1:中國房地產相對收益於2018年2月已觸及其長期趨勢的頂點,但自2021年7月以來一直預期着寬鬆政策的落地。

資料來源:彭博,交銀國際

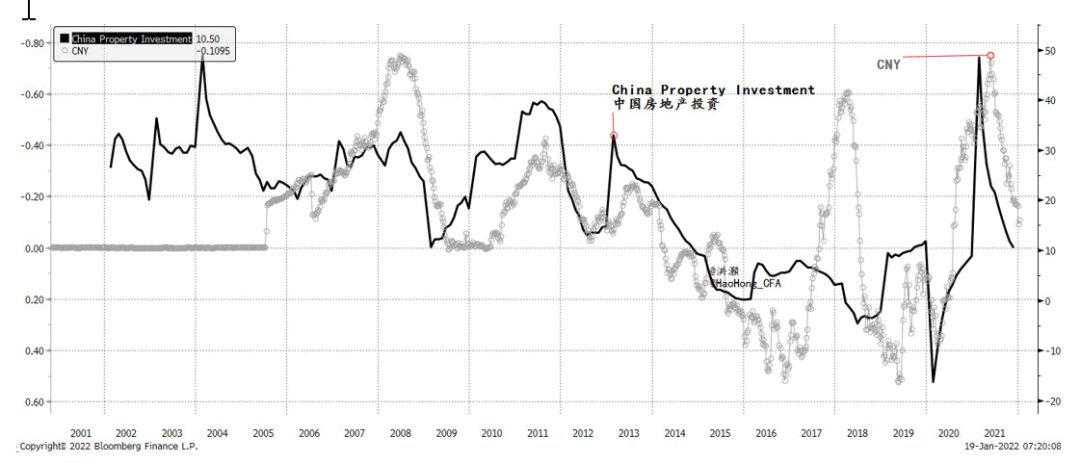

與此同時,人民幣強勢的消退與下行的房地產投資增速並行不悖(圖表2)。鑑於“三紅線”政策依然高懸於頂,房地產投資增長很可能在未來數月裏從去年極高的基數繼續回落,並將穩定在一個較低的水平。隨着美聯儲收緊政策如箭在弦,而中國央行繼續放鬆政策,人民幣很可能會有所走軟。鑑於中美兩國貨幣政策的歷史相關性,大規模寬鬆的政策窗口正在迅速地關閉——否則人民幣將承壓,並有可能引發投機性資本外流。這種迅速關閉的政策時間窗口解釋了爲什麼央行將其寬鬆政策的日程提前,而一些交易員也將爲此而激動,貿然押注於這種寬鬆預期。然而,匯率是一項重要的政策制約,市場預期也往往是朝生暮死的。

圖表2:人民幣和下行的房地產投資增速。

資料來源:彭博,交銀國際

我們的中國經濟週期理論再次得到驗證。中國的經濟短週期時間跨度爲每3至4年,而目前正處於最後的放緩階段(圖表3)。在這一階段,央行將下調存準和利率,投資增速將隨之而減,外儲將見頂而人民幣將走軟。我們在題爲《展望 2022:夕惕若厲》的展望報告中已細緻入微地探討了我們的經濟週期理論對投資的啓示。

總而言之,市場一直在預期中國央行將出臺寬鬆政策,房地產行業反彈至一年高點把這種寬鬆的預期展示得淋漓盡致。此外,隨着美聯儲摩拳擦掌準備加息,央行採取先發制人寬鬆政策的窗口正在迅速關閉。這正是央該會再度成爲交易員密切關注的、綱領性宏觀主題。行迅速行動的原因所在。這種預期將煽動交易員押注諸如大宗商品和債券等對利率敏感的資產。而股市也可能得到短暫的提振。之後,中國經濟短週期的減速和美聯儲的鷹派立場應該會再度成爲交易員密切關注的、綱領性宏觀主題。

圖表3:中國央行貨幣政策週期正處於寬鬆階段。

資料來源:彭博,交銀國際

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of this article is for reference only. It does not constitute an offer, solicitation, recommendation, opinion or guarantee of any securities, financial products or instruments.The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance.