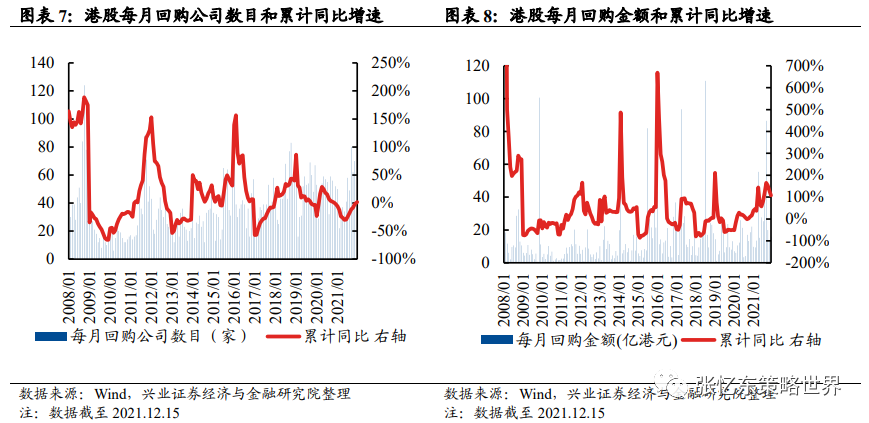

1、港股回購活動明顯升溫

截至12月15日,2021年港股有185家公司回購,累計回購金額達到335.1億港元,創2002年有數據記錄以來的歷史新高;其中下半年有142家公司回購,回購金額達204.3億港元,創半年度新高。行業上,2021年以來資訊科技業、地產建築業、消費業等調整明顯的行業,也是回購的主力行業:從回購公司數目上看,地產建築業46家,非必需性消費業44家,醫療保健業31家,資訊科技業22家;從回購金額上看,資訊科技業爲121億港元,遠遠高於第二名地產建築業的54.6億港元,此外必需消費業(46.2億港元)和非必需消費業(32.2億港元)回購金額同樣排名前列。

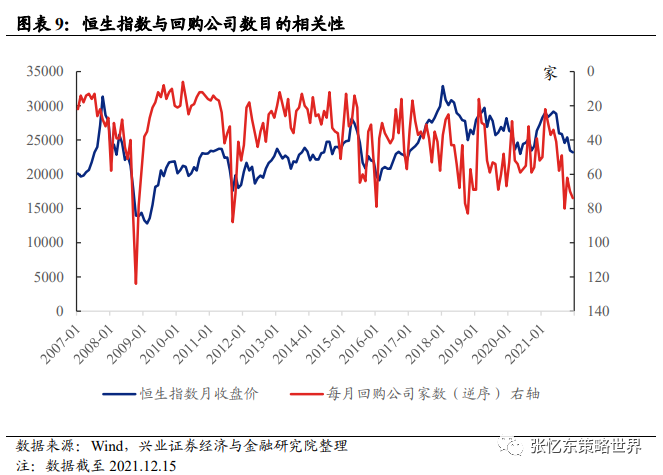

2、以史爲鑑,回購潮可能是未來股價上漲的先行信號

2008年以來港股經歷過五輪公司回購潮,均在熊市中發生,恆生指數價格與公司回購數量呈現負相關走勢,大規模的公司回購往往預示着階段性底部,並且後續均伴隨着一波上漲行情。

-

第一輪明顯回購潮發生在全球金融危機時期,2008年全年港股公司回購金額總計達到175億港幣,恆指全年下跌48.3%。而在接下來的12個月,從2019年1月至2019年12月,恆生指數上漲了52.0%。

-

第二輪迴購潮發生在2011年7月至2012年6月,港股公司共回購121億港幣股票,恆指在這段時期下跌13.2%。在隨後的6個月的時間(2012年7月-2012年12月)上漲16.5%。

-

第三輪迴購潮出現在2014年1月至6月,港股公司累計回購金額100億港元,隨後開啓一波牛市,並於2015年4月恆指突破28000點。

-

第四輪迴購潮出現在2015年7月至2016年12月,累計回購金額409.8億港元,恆指下跌16.2%。而在隨後的13個月,自2017年1月至2018年1月,恆生指數上漲49.5%,並於2018年1月突破33000點。

-

第五輪迴購潮出現在2018年2月至2018年10月,累計回購231.2億港元,恆指累計下跌24.0%,其中2018年10月跌破25000點。隨後的6個月(2018年11月-2019年4月),恆指上漲18.9%。

-

此次回購潮從2021年二季度開始,2021 年下半年隨着港股較大幅度下跌而進入高潮,不到半年時間回購力度已經超過 200 億港元,超過以往歷史任何一個半年度數據。下半年截至 12 月 15 日,恆指已累計下跌了 18.8%。

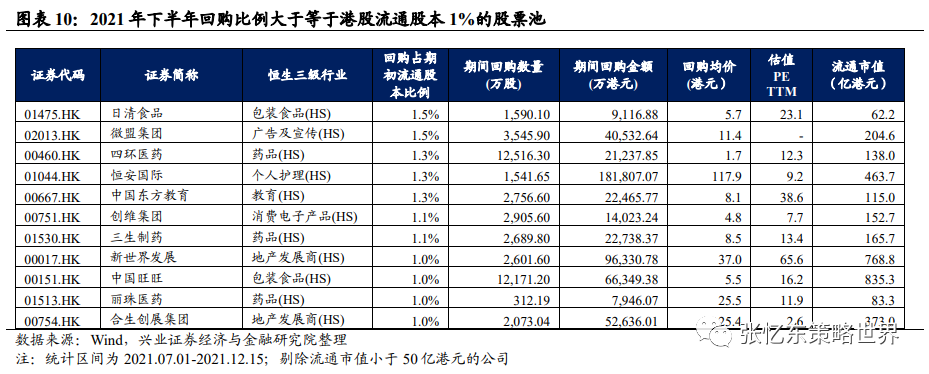

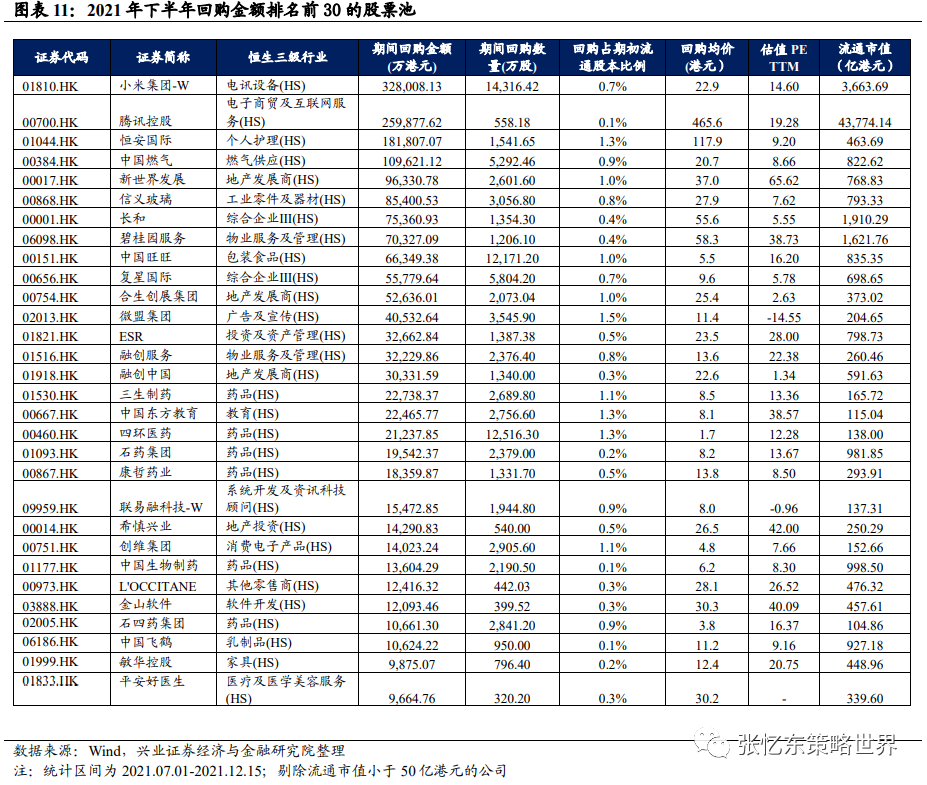

3、哪些公司大規模回購?

港股當前估值較低,大規模的公司回購可以給投資者樹立價值標杆,彰顯公司信心,從而推動公司的價值重塑。因此我們篩選出兩個股票池:1)2021年下半年(截至12月15日)回購比例大於等於港股流通股本1%且流通市值大於50億港元的股票池;2)回購金額排名前30且流通市值大於50億港元的股票池。

風險提示:中、美經濟增速下行;美國持續高通脹,美國貨幣政策提前超預期收緊;大國博弈風險;新冠疫情變異超預期;回購可能也意味着企業由於缺乏好的投資項目而不願意進一步投資,只能選擇用現金來回購股票。

—●●●●—

報告正文

—●●●●—

1、港股回購活動明顯升溫

2021年以來,港股受多重因素影響回調明顯,截至12月15日,恆指跌14.0%,恆生科技跌31.2%;行業上,恆生資訊科技業跌30.9%,醫療保健業跌29.3%,地產建築業跌19.4%,必需消費業跌17.7%。

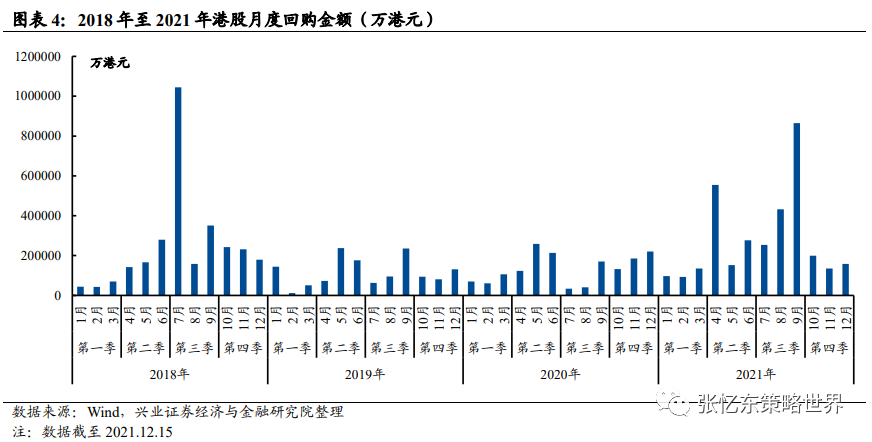

但與此同時,港股回購創歷史新高,彰顯企業信心。截至12月15日,2021年港股有185家公司回購,累計回購金額達到335.1億港元,創2002年有數據記錄以來[1]的歷史新高;其中下半年有142家公司,回購金額達204.3億港元,創半年度新高。行業上,2021年以來資訊科技業、地產建築業、消費業等調整明顯的行業,也是回購的主力行業:從回購公司數目上看,地產建築業46家,非必需性消費業44家,醫療保健業31家,資訊科技業22家;從回購金額上看,資訊科技業爲121億港元,遠遠高於第二名地產建築業的54.6億港元,此外必需消費業(46.2億港元)和非必需消費業(32.2億港元)回購金額同樣排名前列。

[1]數據來源爲Wind終端

2、以史爲鑑,回購潮可能是未來股價上漲的先行信號

2008年以來港股經歷過五輪公司回購潮,均在熊市中發生,恆生指數價格與公司回購數量呈現負相關走勢,大規模的公司回購往往預示着階段性底部,並且後續均伴隨着一波上漲行情。

-

第一輪明顯回購潮發生在全球金融危機時期,2008年全年港股公司回購金額總計達到175億港幣,恆指全年下跌48.3%。而在接下來的12個月,從2019年1月至2019年12月,恆生指數上漲了52.0%。

-

第二輪迴購潮發生在2011年7月至2012年6月,港股公司共回購121億港幣股票,恆指在這段時期下跌13.2%。在隨後的6個月的時間(2012年7月-2012年12月)上漲16.5%。

-

第三輪迴購潮出現在2014年1月至6月,港股公司累計回購金額100億港元,隨後開啓一波牛市,並於2015年4月恆指突破28000點。

-

第四輪迴購潮出現在2015年7月至2016年12月,港股公司累計回購金額409.8億港元,恆指下跌了16.2%。而在隨後的13個月,自2017年1月至2018年1月,恆生指數上漲了49.5%,並於2018年1月突破33000點。

-

第五輪迴購潮出現在2018年2月至2018年10月,港股公司累計回購231.2億港元,恆指累計下跌24.0%,其中2018年10月跌破25000點。隨後的6個月(2018年11月-2019年4月),恆指上漲18.9%。

-

此次回購潮從2021年二季度開始,2021 年下半年隨着港股較大幅度下跌而進入高潮,不到半年時間回購力度已經超過 200 億港元,超過以往歷史任何一個半年度數據。下半年截至 12 月 15 日,恆指已累計下跌了 18.8%。

3、哪些公司大規模回購?

港股當前估值較低,大規模的公司回購可以給投資者樹立價值標杆,彰顯公司信心,從而推動公司的價值重塑。因此我們篩選出兩個股票池:1)2021年下半年(截至12月15日)回購比例大於等於港股流通股本1%且流通市值大於50億港元的股票池(見圖表10);2)回購金額排名前30且流通市值大於50億港元的股票池(見圖表11)。

4、風險提示

中、美經濟增速下行;美國持續高通脹,美國貨幣政策提前超預期收緊;大國博弈風險;新冠疫情變異超預期;回購可能也意味着企業由於缺乏好的投資項目而不願意進一步投資,只能選擇用現金來回購股票。

More Content