港股牛市來了,難道不關注下惠理集團(806.HK)麼?

【交易型機會】

最近港股火爆,成交額首次突破3000億,南下港股通也是蹭蹭蹭的上漲,很多人把目光瞄準了港交所。沒錯,每次港股牛市,港交所必將是收益股之一,因為市場成交更活躍了,而港交所做的就是抽傭的生意。港交所之後,很多人把目光瞄準了港股券商股,比如今天的國泰君安國際,海通國際等等,都是大漲,但是如果這次港股牛市定義為南下資金的牛市的話,那麼香港本地券商可能並不是最受益的。但是有一隻很多朋友不瞭解的港股,是直接受益於股市上漲的。

那就是惠理集團(0806.HK)並且也是滬港通標的。

惠理集團就是一家資產管理公司,2020上半年公佈的半年報顯示管理資產總值是118億美元。

惠理集團創立於1993年2月,公司自成立伊始就運用價值投資專注於亞太地區的資產管理業務。公司的首隻基金“惠理價值基金”於1993年4月成立,初始管理資產規模560萬美元。自1997年至今,謝清海先生一直是公司的單一最大持股股東,葉維義先生一直是公司非執行董事。惠理集團於2007年12月於香港聯合交易所主板上巿(股份編號:806),成為香港第一家上市的資產管理公司。

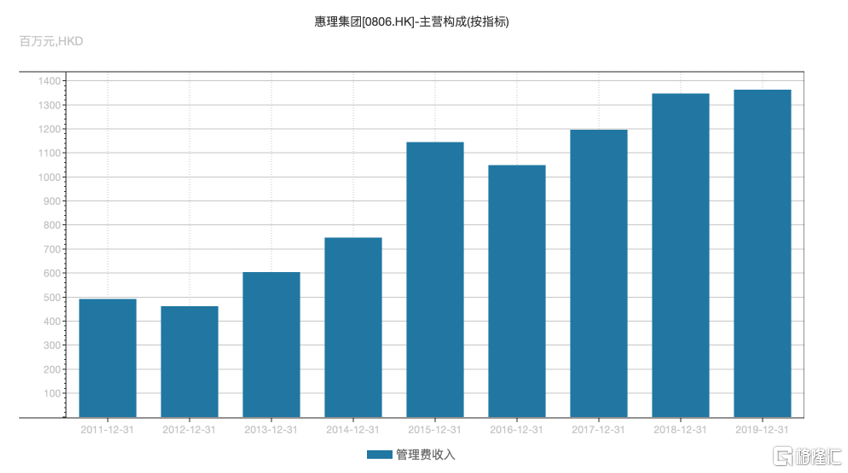

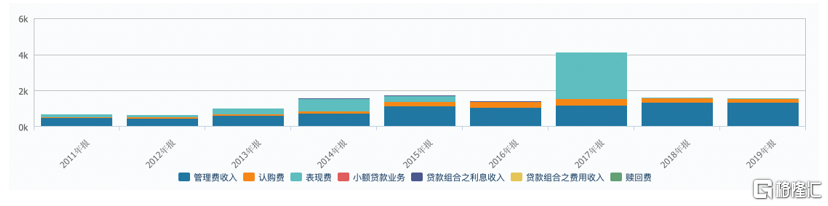

惠理集團在非牛市的行情中,主要收入來源為管理費,佔總收入比重超過80%,牛市的話,表現費會呈幾何倍的增長,這個後面會分析。所管理基金按策略劃分,大約58%為絕對回報偏持長倉基金,簡單理解為多頭基金,剩餘的為固收、另類、量化和ETF。

惠理集團2020上半年管理費收入5.19億港幣,2020上半年平均管理資產規模126億美元,按照7.75的匯率,大約可以算出惠理的平均費率0.5%。隨着港股股市的大漲,惠理管理規模也會隨之上漲,那麼收到的管理費也將水漲船高。而且牛市來了,認購基金的客户也會更多,進一步推升惠理管理規模的上升。

從收入結構上來説,惠理的管理費收入比較穩定,屬於穩定上漲的情況,畢竟這個是和管理規模直接掛鈎的收入,費率大約在0.5%-0.7%之間,費率波動主要是產品類型佔比的不同,債券類型的費率較多頭高0.25%左右。

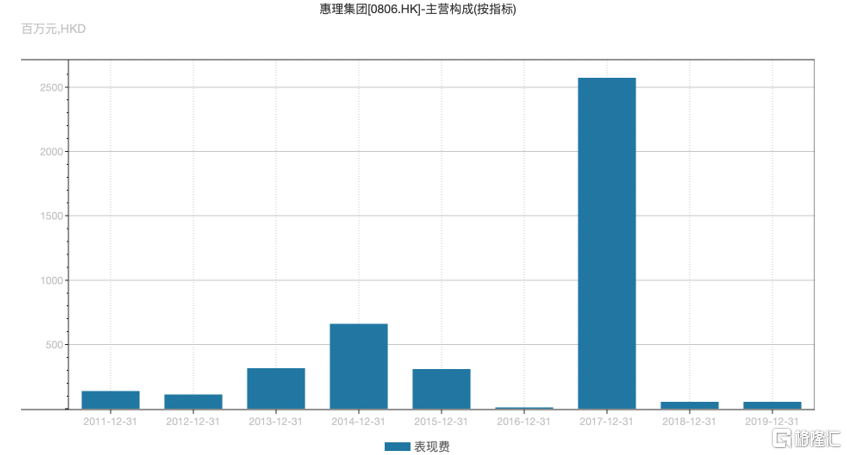

收入波動的大頭來自於表現費,比如2017年持續了一年的大白馬行情,惠理的表現費收入直接從16年的忽略不計到17年的25億多,佔當年總收入超過60%。

疊加在一起就是,在牛市中,惠理的業績彈性是非常誇張的,一方面管理規模上去管理費可以收更多,在牛市行情中,表現費也可以收更多。

從交易的角度,我們把惠理集團的股價和恆生指數進行疊加,基本得到了一個放大版的Beta股,比如15年港股第一次南下資金爭奪定價權時,港股引來了一波牛市,當時惠理集團的股價在段時間內從5塊上漲到了13塊。從2020年3月股市低點之後,恆生指數上漲了30%,惠理集團就上漲了91%。

所以在牛市來臨之際,從股價波動的角度來説,即使我們不瞭解惠理集團的基本面,也完全可以依靠對港股未來牛市的信仰買入惠理集團。

最後,從估值的角度,惠理的估值目前處於歷史最底部。惠理一般市場會用P/AUM來進行估值,在過去的10多年裏,這個數字一般維持在14%左右,但是現在,這個數字只有5%,處於歷史最底部。如果港股牛市可以持續,那麼未來的惠理或許有機會得到估值和業績的雙擊。如果港股牛市也只如15年那樣曇花一現,那麼享受一把泡沫,應該也是可以的。

作為在香港第一家上市的基金公司,公司堅守價值投資的理念,通過穩健而靈活的投資方法,持續為客户創造價值,而良好的長期表現使得投資者在危機時刻更加信賴公司,提升了公司對抗系統性風險的能力。雖然惠理集團的價值實現非常依賴於股票市場的繁榮,而香港市場從2008金融危機以來就一路下滑,這也導致公司的價值無法兑現;但這並不影響公司的內在價值的增長,惠理集團中價值最重要的來源就是管理資產的持續增長,這是核心。

格隆匯聲明:文中觀點均來自原作者,不代表格隆匯觀點及立場。特別提醒,投資決策需建立在獨立思考之上,本文內容僅供參考,不作為實際操作建議,交易風險自擔。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of this article is for reference only. It does not constitute an offer, solicitation, recommendation, opinion or guarantee of any securities, financial products or instruments.The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance.