今日,港A兩市汽車股集體走低。A股方面,截止收盤,力帆股份跌停,江淮汽車跌超4%,北汽藍谷、中國重汽、ST海馬均跌超3%,眾泰汽車、長安汽車、長城汽車等汽車股則隨之而跌。

(行情來源:同花順)

港股方面汽車股亦同步走低,截止收盤,潤東汽車大跌9.64%,正通汽車跌近5%,廣汽集團、雅迪控股、北京汽車皆跌超2%,吉利汽車、和諧汽車等股則紛紛跟跌。

(行情來源:富途)

從消息面上來看,汽車股今日集體走跌的原因主要是源於“車市銷量下滑”這一消息刺激。

6月22日,中國汽車工業協會聯合中國汽車技術研究中心有限公司、豐田汽車公司等機構和公司發佈一份《汽車工業藍皮書》,據數據顯示,2019年中國汽車銷量同比下降8.2%,而新能源汽車更是出現首次下滑的情況,銷量同比下降4.0%。此外,中汽協還發布數據指出2020年汽車銷量再度下滑的現象,預計今年中國汽車銷量同比下降10%至20%。

直面汽車銷量下滑現象

據《汽車工業藍皮書》數據顯示,2019年汽車行業銷量進一步深度下滑,全年累計銷售汽車2576.9萬輛,較上年減少231.2萬輛,同比下降8.2%,降幅比上年擴大5.4個百分點,比2017年的最高峯(2888萬輛)淨減311.1萬輛。

在這其中,乘用車和商用車的銷量均出現了一定程度上的下滑,其中乘用車(廣義)2019年累計銷售2144.4萬輛,同比下降9.6%,而商用車需求好於乘用車,全年商用車銷售432.4萬輛,同比下降1.1%。

其中,乘用車四個細分市場均全線下滑——轎車全年累計銷售1030.8萬輛,同比下降10.7%;SUV銷售935.3萬輛,同比下降6.3%;MPV銷售138.4萬輛,同比下降20.2%;交叉型乘用車銷售40.0萬輛,同比下降11.7%。

商用車方面,2019年商用車四個細分市場雖均處於下滑趨勢,但降幅均較小。其中,中重卡全年累計銷售131.4萬輛,同比微降0.9%,增速雖有下降,但產銷規模仍處於歷史高位;輕卡銷售188.3萬輛,同比微降0.6%;微貨銷售65.3萬輛,同比下降1.8%;客車銷售47.4萬輛,同比下降2.2%。

不過,需要指出的是,雖然乘用車下滑幅度較大,但仍佔據着汽車市場的主導地位。據藍皮書數據顯示,2019年乘用車銷售佔比為83.2%,連續8年超過80%,汽車行業增長依然主要依靠乘用車帶動。

而需要注意的主要還是新能源汽車首次出現銷量下滑的現象。據《汽車工業藍皮書》數據顯示,2019年,中國新能源汽車市場受出現了首次下滑,全年累計銷售120.6萬輛,同比下降4.0%,佔汽車總銷量比例為4.7%,較2018年提升0.2個百分點。

此外,受2020年初新冠疫情的影響,今年中國汽車銷量預計也將有所下滑。據中國汽車工業協會發布數據顯示,今年以來,受新冠疫情影響,我國汽車市場放緩,預計2020年中國汽車銷量將下降10%至20%。

而中國汽車流通協會副祕書長郎學紅在中國汽車流通行業年會上也表示,2020年車市銷量至少還會出現10%的負增長,樂觀估計能夠達到2250萬輛。

綜合以上兩家協會機構的預測可知,今年中國汽車銷量預計將在去年的基礎上再降10%以上。

汽車行業“回暖苗頭”何時至?

不得不説的是,2020年汽車全年銷量有所下滑主要是一季度銷量大幅下滑拖得後腿。據數據顯示,受新冠肺炎疫情影響,我國汽車行業今年一季度產銷量出現大幅下滑,汽車產銷分別為347.4萬輛和367.2萬輛,同比下降45.2%和42.4%。

但實際上,比起今年一季度大幅下滑的汽車銷量,5月份增速慢慢轉正的汽車銷量已透露了市場逐步回暖的現象。

據相關數據顯示,2020年前5月汽車累計銷量795.7萬輛,同比下滑22.6%,其中5月銷量219.4萬輛,同比增長14.5%,連續第2個月正增長,反映出市場在逐步回暖。

其中,乘用車方面,根據中汽協數據,前5月乘用車累計銷量610.9萬輛,降幅收窄至27.4%,其中5月銷量167.4萬輛,同比增長7.0%,由負轉正,這也是2018年7月以來增速首次轉正。此外,乘聯會數據顯示,5月狹義乘用車零售銷量增速也轉正至1.8%,也帶動累計銷量降幅收窄至26.03%。

對此,有行業人士表示,疫情爆發以來(2月至今)乘用車批發和零售銷量增速均逐步好轉,反映出疫情好轉下企業積極復工復產,人民的生產生活已逐步恢復正常,由此帶來的購車和換車需求陸續釋放。

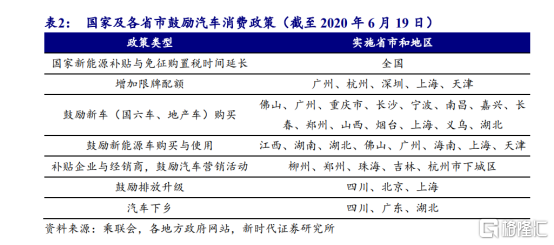

與此同時,中央和各地陸續出台促進汽車消費政策(購車補貼、限購鬆綁等),各大車企也採取了汽車下鄉、官降、打折促銷等活動,消費信心在政策鼓勵和車企促銷等因素疊加下逐步恢復,由此可以預計後續購車需求將逐步緩慢企穩改善。

(圖片來源:新時代證券)

此外,針對於上述表現,中銀證券表示,隨着人們的生活逐漸步入正軌,在政策利好疊加新車型的推出雙重刺激下,汽車終端需求有望復甦。

該機構表示,由於受到疫情衝擊,國內車企將新車型密集推出的時間由二季度推遲到三季度,利好政策疊加新車型推出,有望對衝疫情影響、提振國內市場需求,預計二季度銷量環比好轉,三四季度銷量同比有望重返增長,帶動產業鏈需求增長。

More Content