8月19日晚间,中国中药(00570.HK)发布公告称,截至2019年6月30日止6个月,公司的营业额以及股东应占溢利双双录得增长。

8月20日,该公司的股价早盘高开0.3%后出现跳水一度下跌近3%,此后又遭遇拉升。截至发稿时间,该股上涨2.7%,股价现为3.42港元,目前成交8054.29万港元。

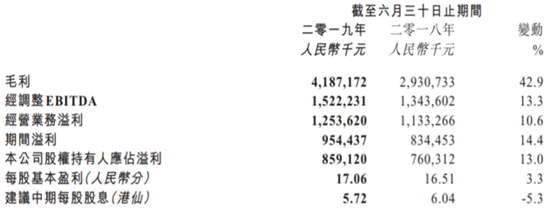

中期净利升13%至8.59亿元

资料显示,中国中药控股有限公司上市于1993年4月,其主要业务为于中国研发、生产及销售中药及医药产品,通过成药、中药配方颗粒、中药饮片、中医药大健康产业、产地综合业务5个经营分部开展。

截至2019年7月10日,该公司的大股东为国药集团香港有限公司,持股比例为32.46%;其背后的实际控制人则是国务院国资委。

(图片来源:Wind)

此次的中期业绩显示,中国中药在报告期内实现营业收入69.37亿元,同比增长27.02%;公司股权持有人应占溢利8.59亿元,同比增长13%,业绩大幅增长主要得益于中药配方颗粒业务继续保持高速稳定增长和成药业务在OTC渠道的发展。

期内,公司的毛利为41.87亿元,同比增长42.9%;期内毛利率为60.4%,比去年同期的53.7%上升6.7个百分点,主要原因是配方颗粒部分品种提取成本下降,以及部分产品提价。

此外,该公司的每股基本盈利为17.06分,拟派中期股息每股5.72港仙。

(图片来源:中国中药公告)

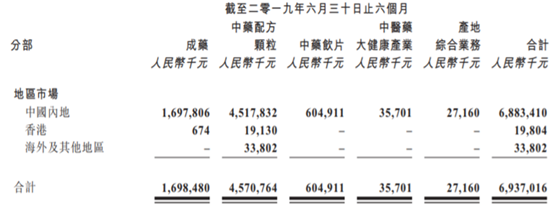

分地区来看,报告期内,该公司在中国内地实现营收68.83亿元,同比增长27.15%,其营收占总营收的比例高达99.22%;香港地区贡献的营收为1980.4万元,同比增长17.27%,占比为0.29%;海外及其他地区贡献的营收为3380.2万元,同比增长8.77%,占比为0.49%。

(图片来源:中国中药公告)

分业务来看,报告期内,中药配方颗粒业务贡献营业额约45.71亿元,同比增长31.1%,该业务的营收占总营业额的65.9%。

这块业务销售收入快速增长主要得益于:(1)配方颗粒的质量可控性及便利性等优势明显,以及卓有成效的学术推广,市场认可度逐步提高,存量客户带来的销售增长约18.2%;(2)顺应市场和医改政策,公司近年不断加大对新客户的开发力度,以进一步加大市场占有率,本期新增客户带来的销售增长约12.9%。

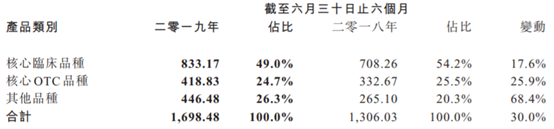

期内,成药业务营业额约16.98亿元,同比增长30%,其收入占总营业额的24.5%,该业务板块的临床渠道及OTC渠道核心品种同比分别增长了17.6%、25.9%。

(图片来源:中国中药公告)

同期,中药饮片业务营业额约6.05亿元,同比下降5.4%,营收占总营业额的8.7%。

该业务板块营业额下降,主要是因为:公司优化业务结构,放弃部分传统低毛利业务,开始提高特色品种及高毛利品种的销售量。新建工厂初期以内部供应为主,磨合生产,为下一步扩大对外销售打下基础。

期内,中医药大健康产业业务营业额约3570.1万元,同比增长41.3%,收入占总营业额的0.5%。

这部分业务营业额上升的主要原因是2018年下半年开始南海国医馆、冯了性城南国医馆、同济堂遵义国医馆、同济堂毕节国医馆陆续开业,佛山冯了性国医馆因开展名医工作室项目,收入有所增长。同时,由于江阴国医馆,业务类型调整,增加了饮片、理疗、成药、参茸贵细销售项目,收入增加。

期内,产地综合业务营业额约2716万元,同比增长828.9%,该业务的营收占总营业额的0.4%。

产地综合业务营业额大幅上升,主要是因为部分产地综合业务公司陆续完成筹建工作,开始正常对外销售,摆脱了去年同期负毛利的状态。同时本期产地综合业务公司获得了约人民币2757.5万元的政府补助收入,消除了部分筹建初期费用开支对净利润的影响。

机构怎样看待后市?

近期也有一些券商机构发表了对于该上市公司未来发展前景的看法:

中金公司认为,中国中药1H19业绩符合预期,维持2019年/2020年每股盈利预测0.34元/0.40元,对应同比增长18%/19%。当前股价对应2019/2020年8.8倍/7.4倍市盈率,维持跑赢行业评级和4.62港元目标价,对应12.2倍2019年市盈率和10.3倍2020年市盈率,较当前股价有39%的上行空间。

而在此前,银河国际发表研究报告称,将中国中药2019/20年盈利预测下调7%/9.5%,将目标价从6.3港元(历史平均:16倍2019年市盈率)下调至4.2港元(11倍2019年市盈率,比历史平均低1个标准差)。但是考虑到目前9.5倍2019年市盈率已较历史平均值低出超过一个标准差,故维持「增持」评级。

More Content

Physical Store(set to open in Q2 2025)

Address:

Shop LMC 307, 3/F, Lok Ma Chau MTR Station, Lok Ma Chau

Opening Hour:

9am - 9pm (Mon - Sat)

10am - 6pm (Sun and Public Holiday)

(set to open in Q2 2025)